Q1. What does Recorded Future actually cost in 2026, and why is the price never on the website?

Recorded Future is quote-only in 2026. Verified Vendr transaction data shows entry contracts start at $40,000 to $60,000 for a single module, mid-market deployments land between $75,000 and $200,000 ACV across three to five modules, and full-suite enterprise contracts run $250,000 to $500,000+. Pricing is driven by package selection, organization size, usage volume (API calls, enrichment scope), and services tier, not seat counts under the new 2026 unlimited-user model.

A CISO at a 4,000-person fintech in New York once told me on a 2 a.m. bridge call, “I pay Recorded Future six figures a year, and my Tier 1 still cannot tell me if we are specifically at risk.” That gap, the one between News and Intelligence, is the real cost story. If you want to model the alternative side by side, our SOC cost calculator walks through the math on a flat-rate basis.

Negotiating a renewal right now?

Talk to a team that benchmarks these deals every week.

💰 What buyers actually sign in 2026

| Tier | Typical ACV | What you get |

|---|---|---|

| Entry / single module | $40K to $60K | One solution, capped API calls |

| Mid-market bundle | $75K to $200K | 3 to 5 modules, Intelligence Graph access |

| Full-suite enterprise | $250K to $500K+ | All four solutions, Elite tier services |

| Payment Fraud add-on | $50K to $100K | Standalone, financial institutions only |

Recorded Future officially confirmed in April 2026 that all packages now ship with unlimited users and unlimited integrations. That sounds generous until you realise the meter just moved, from seats to API calls and enrichment volume. For a deeper read on this shift, see our MDR price guide.

The four pricing variables decoded

The quote you receive is shaped by four levers, in this order:

- Package selection (Core, Professional, or Elite).

- Organisation size, measured by employee count and revenue band.

- Usage volume, mainly API calls and the breadth of Intelligence Graph enrichment per query.

- Services tier, including dedicated Intelligence Services analysts and threat hunting hours.

The API ceiling is the trap. ⚠️ I have watched mid-market teams burn through their query allotment by week three of a quarter, then sit in a renewal call where the “uplift” looks suspiciously like the original quote plus 22%.

Why the price never lives on the website

Recorded Future withholds list pricing because the bundled-quote model preserves their commercial leverage. Every quote is custom, every renewal is a fresh negotiation, and the buyer rarely has a comparable peer benchmark. That opacity is a feature for the seller, and a tax on the buyer.

In our experience walking customers through MDR procurement, transparent flat-rate pricing changes the conversation. We publish ours on our MDR pricing page: $11 to $15 per endpoint per month, no per-API-call surprises. The structural contrast matters more than the dollar figure, because predictable pricing means predictable security planning.

Q2. How do the new 2026 Four Solutions and Three Packages (Core, Professional, Elite) actually map to your SOC use cases?

Recorded Future’s April 2026 architecture bundles four solutions, Cyber Operations, Digital Risk Protection, Third-Party Risk, and Payment Fraud Intelligence, into three tiers: Core (Cyber Ops + DRP), Professional (adds Attack Surface Intel and autonomous threat hunting), and Elite (full cross-domain coverage including Third-Party Risk). All packages include unlimited users and unlimited integrations on the Intelligence Graph (1.2M sources, 26B entities). Payment Fraud Intelligence remains a standalone add-on for financial institutions.

Recorded Future’s April 2026 architecture bundles four solutions into three tiers, all riding the same Intelligence Graph (1.2M sources, 26B entities) with unlimited users and integrations. That sounds clean on a slide. In a real SOC, the question is which tier actually feeds your detections. For background, our team’s guide to MDR services walks through how detection feeds become operational signal.

The architecture in plain English

Think of it like a cable TV bundle. Core gets you the basics, Professional adds premium channels, and Elite throws in the sports package. The Intelligence Graph is the cable line itself, and every tier rides on it.

Solution-to-domain mapping

- Cyber Operations: indicators, malware families, threat actor TTPs (Tactics, Techniques, and Procedures), the bread and butter for SOC analysts.

- Digital Risk Protection (DRP): brand abuse, leaked credentials, dark-web mentions of your domain.

- Third-Party Risk: continuous monitoring of vendor security postures.

- Payment Fraud Intelligence: card BIN compromise, fraud rings, mule accounts, mostly relevant to banks and PSPs.

🎯 Tier-to-capability deltas

| Capability | Core | Professional | Elite |

|---|---|---|---|

| Cyber Operations | ✅ | ✅ | ✅ |

| Digital Risk Protection | ✅ | ✅ | ✅ |

| Attack Surface Intelligence | ❌ | ✅ | ✅ |

| Autonomous Threat Hunting | ❌ | ✅ | ✅ |

| Third-Party Risk | ❌ | ❌ | ✅ |

| Unlimited users | ✅ | ✅ | ✅ |

A SOC Director at a 4,000-person SaaS company asked me last quarter, “If I buy Professional, do my Tier 1 analysts touch Attack Surface Intelligence daily, or does it sit in a separate console?” That is the right question. ⚠️ Recorded Future ships the data, but the integration into your SIEM detection pipeline is your team’s homework. In our experience hardening SOCs at UnderDefense, that homework eats 40% of the value of any new tier upgrade in Year 1.

Which buyer profile fits which tier

A 1,200-person SaaS company with a small SOC and no formal threat hunting program rarely needs Elite. Core covers triage enrichment and brand monitoring, which is roughly 70% of what their analysts actually consume.

A 6,000-person manufacturer with global supply chains and a real third-party blast radius gets disproportionate value from Elite, because the Third-Party Risk module is genuinely hard to replicate with free sources.

A regional bank or PSP should treat Payment Fraud Intelligence as the anchor and bolt the rest on conservatively. For tooling parallels, our MDR for Financial Services page covers the operational pattern.

The “data island by tier” problem

Here is what bothers me, and I might be wrong, but I see it a lot. Each tier is a data island. ❌ Your Cyber Ops feed does not automatically correlate with your endpoint telemetry, your identity provider, or your SIEM detections. Recorded Future tells you what is out there, then hands you a Slack-style alert and walks away.

In our experience hardening SOCs at UnderDefense, the unified UnderDefense Agentic AI SOC platform ingests Recorded Future outputs alongside identity, EDR, and cloud signals, then runs the correlation. ✅ That is the “Iron Man Suit” piece, the platform augments analyst judgement instead of replacing it with another report.

“The biggest win for me was getting actual control over our security alerts. Before the guys from UD stepped in, we were getting bombarded with alerts from all our security tools. Their team cleaned up our configurations and got the noise under control within the first week.”

— Verified User, Marketing and Advertising UnderDefense G2 – Verified Review

Q3. What does each of the eight modules actually do, what does it cost à la carte, and which ones are worth the surcharge?

Threat Intelligence anchors the platform at $50K to $150K. Add-on modules cluster between $20K and $80K annually: Brand Intelligence ($30K to $80K), SecOps Intelligence ($30K to $80K), Vulnerability Intel ($25K to $70K), Attack Surface Intel ($25K to $70K), Identity Intel Workforce ($25K to $60K), Third-Party Intel ($25K to $60K), and Geopolitical Intel ($20K to $50K). Payment Fraud Intelligence runs $50K to $100K standalone. Bundling consistently delivers 20% to 35% better per-module economics than incremental add-ons at renewal.

How to read these ranges

The low end of each band is what well-prepared mid-market buyers (1,000 to 3,000 employees) sign with a competitive RFP. The high end is what under-leveraged enterprise buyers pay when they renew without benchmarking. The delta is almost always procurement discipline, not feature parity. Our MDR buyers guide covers the same procurement discipline applied to MDR contracts.

⭐ The module-by-module matrix

| Module | What it actually does | Range (USD/yr) | Worth it when… | Overpriced when… |

|---|---|---|---|---|

| Threat Intelligence | Core IOC, malware, actor enrichment | $50K to $150K | Tier 2 analysts use it daily | You already have CTA + MISP coverage |

| Brand Intelligence | Domain spoofing, leaked creds, dark web | $30K to $80K | Consumer brand, public-facing | Your MDR ships leak-check free |

| SecOps Intelligence | Pre-tuned SIEM detections | $30K to $80K | Detection engineering is thin | Mature detection-as-code shop |

| Vulnerability Intel | Risk-prioritised CVE feed | $25K to $70K | Patching team needs ranking | CISA KEV satisfies 60% of triage |

| Attack Surface Intel | External asset discovery | $25K to $70K | M&A heavy, sprawling cloud | M365 OAuth audit covers Shadow IT |

| Identity Intel Workforce | Exposed employee credentials | $25K to $60K | No HIBP enterprise tier | You already use HIBP + Entra ID |

| Third-Party Intel | Vendor risk continuous monitoring | $25K to $60K | Regulated, 200+ vendor footprint | Annual SIG questionnaires suffice |

| Geopolitical Intel | Nation-state risk briefings | $20K to $50K | Global ops, exec protection | US-only mid-market |

Top three “most worth it” modules

✅ Threat Intelligence (anchor, hard to replicate quickly), Vulnerability Intelligence (real ranking signal beyond CVSS), and SecOps Intelligence for teams without a detection engineering bench.

Two “overpriced for most buyers”

❌ Identity Intelligence Workforce duplicates Have I Been Pwned plus Microsoft Entra ID alerts for most enterprises. ❌ Geopolitical Intelligence reads like a McKinsey briefing. It is valuable for a Fortune 100 board, and expensive noise for a 2,000-person SaaS. The same pattern shows up across the field, which is why our top threat detection tools roundup uses outcome density as the ranking metric.

What real buyers say about black-box TI and MDR pricing

“We received little value from ArcticWolf. The product offered little visibility… Anything you want to look at or changes you need to make in the product must go through their engineering team.”

— Matt C., Manager, Cybersecurity Services Arctic Wolf – G2 Verified Review

“Over the past few years, we’ve undergone several external penetration tests, and during these assessments, Red Canary was not able to identify the malicious activity while the tests were ongoing.”

— Verified User in Insurance Red Canary – G2 Verified Review

Working with 500+ security teams, what I have noticed is that buyers undervalue what they already own and overpay for what is glossy. UnderDefense Agentic AI SOC ships free leak-check and dark-web monitoring as core platform capability, which is most of what entry-level Brand Intelligence delivers, without the $30K to $80K surcharge.

“It’s reassuring to know they’re always watching for threats, and it doesn’t cost a fortune… The platform works really well with our other security tools.”

— Serhii B., CISO UnderDefense G2 – Verified Review

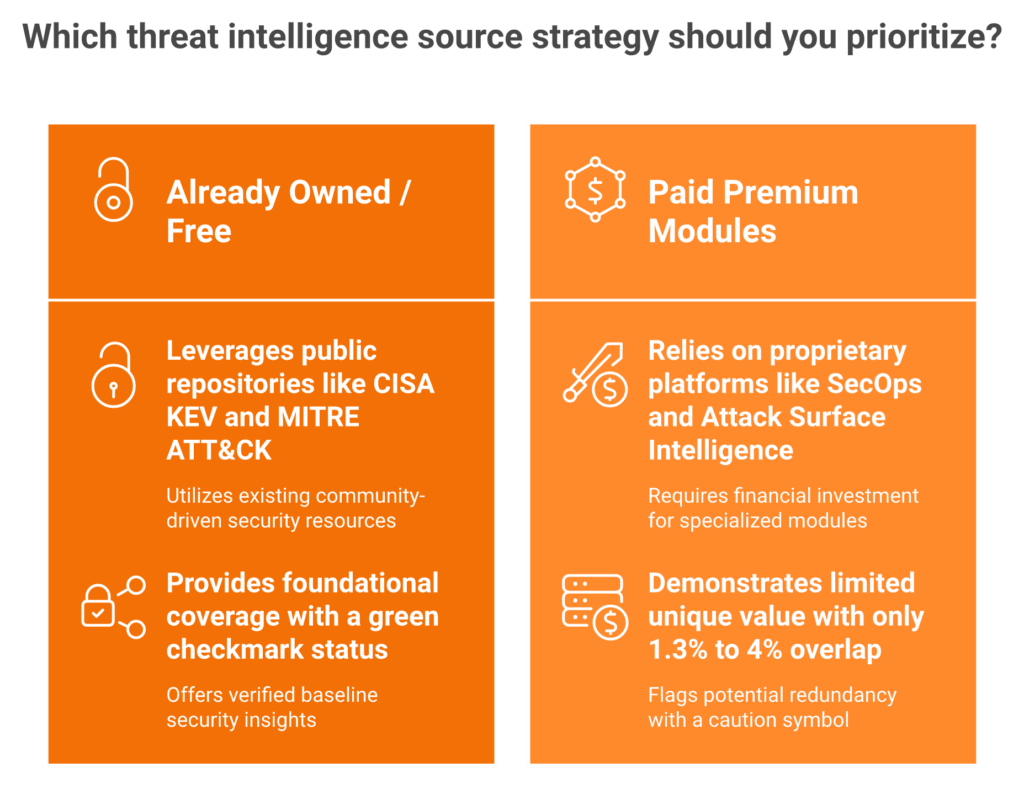

Q4. What free, open-source, or already-owned alternatives should you audit before buying any Recorded Future module?

Before purchasing Recorded Future modules, audit five free or already-owned sources: CISA KEV Catalog substitutes 60% of Vulnerability Intelligence triage logic; MITRE ATT&CK enrichment is free in most SIEMs; M365/Google OAuth consent log audits surface Shadow IT for free in place of Attack Surface Intel; the Cyber Threat Alliance shares adversary playbook STIX intelligence across 34 member vendors at zero cost; and MISP delivers community IOC sharing. Run this audit first, because it can eliminate two to three modules from the quote.

🔍 The Monday-morning audit checklist

- CISA Known Exploited Vulnerabilities (KEV) Catalog

- Replaces or augments: Vulnerability Intelligence module.

- Audit step: pull the KEV CSV, join against your asset inventory in your SIEM, and build a “KEV-present” dashboard.

- Coverage gap: KEV lags a few days behind in-the-wild exploitation, so high-velocity threat actors may still justify paid VI.

- MITRE ATT&CK enrichment

- Replaces or augments: SecOps Intelligence pre-tuned detections.

- Audit step: enable native ATT&CK tagging in Splunk, Sentinel, or Elastic. Most SIEMs ship this free in 2026.

- Coverage gap: ATT&CK gives the framework, not the per-actor playbook depth.

- Microsoft 365 / Google Workspace OAuth consent log audit

- Replaces or augments: Attack Surface Intelligence (Shadow IT discovery).

- Audit step: export OAuth consent grants from Entra ID, flag unsanctioned third-party apps, and review monthly.

- Coverage gap: misses unmanaged personal-device SaaS not connected to corporate identity.

- Cyber Threat Alliance (CTA) STIX feeds

- Replaces or augments: Threat Intelligence module.

- Audit step: if your EDR or NGFW vendor is one of the 34 CTA members, you already receive shared adversary playbook intelligence at no extra cost.

- Coverage gap: CTA depth is broad but not as curated as a paid analyst-written report.

- MISP (Malware Information Sharing Platform)

- Replaces or augments: Threat Intelligence IOC enrichment.

- Audit step: stand up a MISP instance, subscribe to community feeds, and pipe into your SIEM.

- Coverage gap: requires a half-FTE to maintain, so it is not free in labour terms.

The 1.3% to 4% overlap problem

Bouwman et al., USENIX Security 2020, “A Different Cup of TI?”, measured that only 1.3% to 4% of indicators overlap across paid commercial threat intelligence feeds. Read that again. Two vendors selling premium TI to the same buyer are agreeing on a few percent of what matters. That finding is six years old now, and it still holds, because the underlying economics of intel collection have not changed.

Why this matters for your renewal

⏰ Most buyers I talk to have never run this audit. They renew Recorded Future, Mandiant, or Flashpoint on autopilot, then fund the gap with a separate MDR contract. The audit takes one analyst week, and routinely strips two to three modules out of the quote. For a parallel exercise on the MDR side, see our why businesses switch providers breakdown.

The AI accuracy ceiling read

In our experience of building SOC teams across global enterprises, AI-generated TI summaries are correct about 30% of the time on novel threats. That number is fine for triage augmentation, and dangerous for autonomous decisions. Pair every paid feed with a human validation layer, or accept the false-positive tax. Our take on this trade-off is in does AI kill or save SOC.

💸 What my experience of shipping UnderDefense Agentic AI SOC tells me is this: “AI is whatever machines haven’t done yet.” Buyers undervalue the M365 E5 entitlements, OAuth consent logs, and CTA feeds they already own, then overpay for new TI modules that solve 30% of the same problem. Audit first. Buy second. ✅

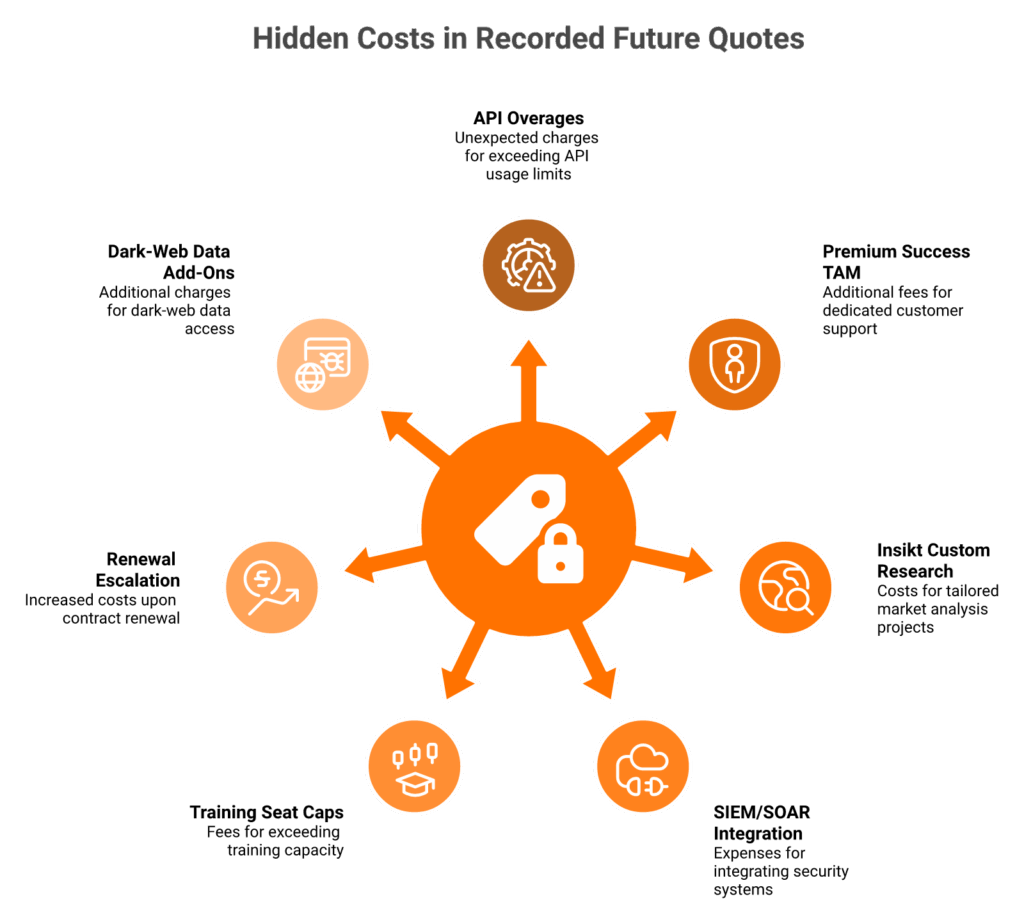

Q5. What hidden fees and add-ons ambush buyers after they sign?

Seven hidden costs consistently ambush Recorded Future buyers: API overages priced separately with no published cap, Premium Success TAM at 10% to 20% of base ACV, Insikt Group custom research at $50K to $150K, custom SIEM/SOAR integration professional services at $15K to $40K, advanced training capped at 15 seats per year, renewal escalation defaulting to 5% to 7% annually, and dark web data purchases scoped as discrete add-ons. Vendr data shows scope-confirmation before signing avoids $15K to $75K in unexpected costs.

A CFO at a 3,500-person SaaS company once told me, “We thought we bought a platform. We actually bought a meter.” That is the trap, and it is avoidable. Our MDR buyers guide walks through the same trap on the MDR side, with the exact clause language to scrub.

The seven gotchas, with negotiation scripts

- ⚠️ API overages with no published cap

- Reality: overage billing kicks in silently when query volume spikes, often during a live incident.

- Impact: $5K to $25K per quarter in surprise charges.

- Script: “Cap our API overage at 10% of base ACV with notification at 80% threshold.”

- 💸 Premium Success TAM (Technical Account Manager)

- Reality: advisory hours are limited (commonly 6 sessions/year), and priced at 10% to 20% of base ACV.

- Impact: $20K to $80K per year for a $200K ACV deployment.

- Script: “Bundle TAM into base fee. Our deal is north of $200K ACV.”

- Insikt Group custom research

- Reality: bespoke threat actor reports are scoped per engagement.

- Impact: $50K to $150K per project.

- Script: “Include two custom Insikt reports per year in Year 1 to prove value.”

- Custom SIEM/SOAR integration professional services

- Reality: out-of-box integrations are free, but custom Splunk, Sentinel, or Cortex XSOAR work is billed.

- Impact: $15K to $40K per integration.

- Script: “Lock integration PS rate at $X per hour, capped at 80 hours.”

- Advanced training seat caps

- Reality: training entitlements are typically capped at 15 seats per year.

- Impact: $1.5K to $3K per additional seat.

- Script: “Expand to 30 training seats annually, no additional fee.”

The renewal and dark-web traps

- ⏰ Renewal escalation default

- Reality: contracts default to 5% to 7% annual price increases unless negotiated.

- Impact: $35K to $280K over three years on a $250K starting ACV.

- Script: “Cap escalation at 3% with right to benchmark against Vendr median.”

- 💰 Dark web data purchases

- Reality: certain dark-web datasets and credential dumps are scoped as discrete add-ons rather than included.

- Impact: $20K to $60K each.

- Script: “Include credential leak feed and one dark-web marketplace dataset in base.”

The “time is the currency of the cloud” angle

API throttling during a live incident is operationally catastrophic. A 15-minute delay in correlating threat intelligence data is the difference between containment and a board disclosure under SEC Item 1.05. ❌ This is the part the salesperson does not mention in the pitch. For a parallel read on response speed, see how our SLA in cybersecurity framework defines 2-minute Alert-to-Triage and 15-minute escalation for critical incidents.

Working across 500+ customer environments, what I have noticed is that buyers who walk into renewal with documented Vendr benchmarks and a parallel POC scoped strip $15K to $75K from their first-year quote. That single procurement discipline pays for the audit work three times over. Our why businesses switch providers piece documents the same pattern across MDR renewals.

“An Expensive Blackbox and Horrible Partner… We received little value from ArcticWolf. Anything you want to look at or changes you need to make in the product must go through their engineering team.”

— Matt C., Manager, Cybersecurity Services Arctic Wolf – G2 Verified Review

“It’s reassuring to know they’re always watching for threats, and it doesn’t cost a fortune.”

— Serhii B., CISO UnderDefense G2 – Verified Review

Q6. What does a real 3-year TCO and renewal-year inflation curve look like at 50, 200, and 500 analysts?

A 50-analyst Core deployment with Vulnerability Intelligence runs roughly $472K over three years ($3,146 per seat per year blended). A 200-analyst Professional deployment with Third-Party and Identity Intelligence reaches around $1.14M ($1,895 per seat per year). A 500-analyst Elite deployment with the full module suite hits around $2.36M ($1,572 per seat per year). Year 1 spikes from one-time onboarding, and Year 3 reflects a 3% negotiated escalation cap. Buyers who fail to negotiate the cap face 5% to 7% default escalation, adding $35K to $280K over three years.

Methodology and assumptions

Modelling assumptions, applied uniformly across all three sizes:

- 3% negotiated annual escalation cap (vs 5% to 7% default).

- 15% Premium Success TAM uplift on Year 1 base ACV.

- 5% API usage buffer on Years 2 and 3.

- One-time onboarding professional services in Year 1 only.

- Inputs derived from Vendr Marketplace transaction history (May 2026).

For a like-for-like flat-rate model, our SOC cost calculator uses the same assumption discipline applied to AI SOC plus Human Ally pricing.

50-analyst Core deployment

| Year | Base ACV | TAM (15%) | API Buffer | One-time PS | Annual Total |

|---|---|---|---|---|---|

| 1 | $120K | $18K | $0 | $20K | $158K |

| 2 | $123.6K | $18.5K | $6K | $0 | $148.1K |

| 3 | $127.3K | $19.1K | $6.2K | $0 | $152.6K |

| 3-yr TCO | ~$458.7K |

200-analyst Professional deployment

| Year | Base ACV | TAM | API Buffer | One-time PS | Annual Total |

|---|---|---|---|---|---|

| 1 | $300K | $45K | $0 | $35K | $380K |

| 2 | $309K | $46.4K | $15K | $0 | $370.4K |

| 3 | $318.3K | $47.7K | $15.5K | $0 | $381.5K |

| 3-yr TCO | ~$1.13M |

500-analyst Elite deployment

| Year | Base ACV | TAM | API Buffer | One-time PS | Annual Total |

|---|---|---|---|---|---|

| 1 | $600K | $90K | $0 | $50K | $740K |

| 2 | $618K | $92.7K | $30K | $0 | $740.7K |

| 3 | $636.5K | $95.5K | $31K | $0 | $763K |

| 3-yr TCO | ~$2.24M |

The renewal escalation curve

📊 The hidden delta is the escalation rate. On a $300K starting ACV, the Year 3 cost difference between 3% and 7% escalation is $25.2K, and the cumulative 3-year delta is $63K. On a $600K Elite contract, the same comparison balloons to $126K over three years. Our cybersecurity budget 2026 piece shows how to defend that escalation cap to a CFO.

Reframing TCO as a Delivery-Model Cost Matrix

In our experience hardening SOCs at UnderDefense, “proving breach prevention ROI” from a TI feed alone is mostly theatre. The 2025 IBM Cost of a Data Breach report found global average breach cost rose to $4.88M. That denominator is too noisy to credibly attribute to one feed.

The honest TCO comparison is delivery-model versus delivery-model. A unified MDR that ingests the same threat intelligence, correlates it with EDR and identity, and acts in 2 minutes flat-rates closer to $11 to $15 per endpoint per month. For a 5,000-endpoint enterprise, that is $660K to $900K annually with response built in. Our published MDR pricing page shows the per-tier breakdown.

What my experience of shipping UnderDefense Agentic AI SOC tells me is this: ✅ flat pricing is not just cheaper, but structurally honest. You can budget it, defend it to a board, and renew it without re-litigating the meter every year.

Hidden fees adding up faster than expected?

Get a plain-English breakdown tailored to your environment.

Q7. How does Recorded Future stack up against UnderDefense Agentic AI SOC, Mandiant, CrowdStrike Falcon Intel, Anomali, Flashpoint, and Intel 471 on price-to-outcome?

UnderDefense Agentic AI SOC flips the model from “data feed” to “unified AI SOC + Human Ally” on flat-rate pricing with 2-minute Alert-to-Triage and autonomous response. Recorded Future ($50K to $500K+) and Mandiant Advantage ($50K to $600K) sit in the same premium feed tier. CrowdStrike Falcon Intelligence ($15 to $40 per endpoint) wins if you are already on Falcon EDR. Anomali, Flashpoint, and Intel 471 land at $30K to $300K, optimised for feed aggregation, dark-web, and finished cybercrime intel respectively.

The price-to-outcome matrix

| Vendor | Entry / Mid / Enterprise | Key differentiator | When it beats Recorded Future |

|---|---|---|---|

| UnderDefense Agentic AI SOC | $11 to $15 per endpoint/mo flat | Unified AI SOC + Human Ally, 2-min Alert-to-Triage | Need response, not reports |

| Recorded Future | $50K / $200K / $500K+ | Intelligence Graph (1.2M sources) | Pure CTI shop, large analyst bench |

| Mandiant Advantage | $50K / $250K / $600K | Frontline IR-derived intel | Active nation-state targeting |

| CrowdStrike Falcon Intel | $15 to $40 per endpoint | Native Falcon EDR integration | Already on Falcon |

| Anomali | $30K / $80K / $200K | Feed aggregation (ThreatStream) | Multi-feed normalisation |

| Flashpoint | $40K / $120K / $300K | Dark-web HUMINT depth | Fraud and physical security |

| Intel 471 | $35K / $100K / $250K | Finished cybercrime intel | Underground actor tracking |

For a broader vendor field on the MDR side, our MDR vendors list 2025 and CrowdStrike vs SentinelOne breakdown apply the same outcome-per-dollar lens.

Recorded Future and Mandiant: the premium feed tier

Both anchor on breadth. Recorded Future leads on aggregation and graph correlation. Mandiant leads on incident-response-derived intel because Google now owns the IR practice. Either runs $200K to $600K for a serious deployment.

CrowdStrike Falcon Intelligence

If your endpoints already run Falcon, the per-endpoint Intel uplift is the cheapest path to baseline CTI. ❌ The catch is vendor lock-in. The intel is only as portable as your willingness to stay on Falcon EDR. See our CrowdStrike pricing 2026 breakdown for the full module map.

Anomali, Flashpoint, and Intel 471

Anomali shines as a feed-of-feeds aggregator if you already pay for three or more commercial sources. Flashpoint earns its premium when fraud, physical security, or insider threat are board-level concerns. Intel 471 specialises in finished cybercrime intelligence, which suits financial services and law enforcement use cases.

The Cyber Threat Alliance structural challenge

The CTA shares adversary playbook intelligence across 34 member vendors at zero cost using STIX. That structurally undercuts proprietary feed pricing because the same indicators often flow through your existing EDR or NGFW vendor anyway.

The 2-minute Alert-to-Triage difference

In our experience of building SOC teams across global enterprises, the bottleneck is rarely “more data,” but the gap between detection and action. UnderDefense Agentic AI SOC runs at a 2-minute Alert-to-Triage SLA with 15-minute escalation for critical incidents, and autonomous response actions like credential resets and ticket creation. ⚡ That is the “Finish” stage feed-only platforms simply do not provide. Our MDR service page documents the exact response workflow.

“Underdefense is a great choice for teams like ours that are short on resources. It automates many tasks, plus, with 247 monitoring, we know we’re always protected… I used to work with many MDR solutions in the past, and so far Underdefense is the best one!”

— Inga M., CEO UnderDefense G2 – Verified Review

“Lack of true remediation in the response, costing us significantly in resources and introducing risks in security.”

— VP of Technology Arctic Wolf – Gartner Verified Review

Less theatre, more throughput. Less black box, more blue team.

Q8. What are the highest-leverage negotiation moves and contract red flags before you sign or renew?

Seven moves consistently unlock 20% to 40% off the initial quote: a 24- or 36-month term for 15% to 30% lower annual cost, a 3% or flat renewal escalation cap, Premium Success TAM bundled into base fee at $200K+ ACV, pre-negotiated module-expansion pricing, a 30-day auto-renewal opt-out window, an itemised order form per SKU, and Q4 fiscal-year-end timing. Five red flags to scrub: bundled-quote opacity, 60- to 90-day auto-renewal traps, missing termination-for-convenience, vague SLA language, and limited data portability for Insikt reports.

List A: Seven negotiation moves

- ⭐ Multi-year term commitment

- Why it works: predictable revenue is worth a 15% to 30% discount to the AE.

- Script: “We will commit 36 months if you discount Year 1 by 25% and cap escalation at 3%.”

- Likely concession: 18% to 22% off Year 1 ACV.

- Renewal escalation cap

- Why it works: default 5% to 7% compounds invisibly.

- Script: “Maximum 3% annual escalation, written into the order form.”

- Likely concession: 3% to 4% cap.

- 💰 TAM bundled into base

- Why it works: TAM economics flip favourably above $200K ACV.

- Script: “Premium Success bundled, no separate SKU, for any ACV above $200K.”

- Likely concession: full bundle at Elite tier.

- Pre-negotiated module expansion

- Why it works: locks in pricing before next year’s “uplift.”

- Script: “Lock add-on module pricing at today’s rate for 24 months.”

- Likely concession: 12-month price lock standard.

- ⏰ 30-day auto-renewal opt-out

- Why it works: industry standard auto-renewal is 60 to 90 days.

- Script: “30-day notice window, written into termination clause.”

- Likely concession: 45 days commonly granted.

Moves 6 and 7

- Itemised order form per SKU

- Why it works: surfaces the hidden bundled-quote math.

- Script: “Line-item every module, integration, and TAM hour separately.”

- Likely concession: usually granted, exposes negotiation surface.

- Q4 fiscal-year-end timing

- Why it works: AE quota pressure peaks in late January (Recorded Future’s fiscal close).

- Script: “Final approval contingent on signing by January 31.”

- Likely concession: an additional 5% to 10% discount.

For a parallel set of plays on the MDR side, our 2026 cybersecurity budget playbook gives the CFO-ready language.

List B: Five contract red flags to scrub

❌ Bundled-quote opacity. Risk: $20K to $80K of unjustifiable line items. Demand: “Itemise every SKU, integration, and service hour with unit economics.”

❌ 60- to 90-day auto-renewal trap. Risk: missing the window forces a full renewal cycle. Demand: “Auto-renewal limited to 30 days notice, with email confirmation required.”

❌ Missing termination-for-convenience. Risk: locked into a non-performing platform for the full term. Demand: “Termination for convenience with 90-day notice and pro-rata refund.”

❌ Vague SLA language. Risk: no recourse on platform downtime or data lag. Demand: “99.9% uptime SLA, data freshness under 4 hours, with service credits.” Our SLA in cybersecurity piece outlines defensible SLA structures.

❌ Limited data portability for Insikt reports. Risk: cannot extract analyst-grade research after termination. Demand: “Right to export all Insikt reports and Intelligence Graph queries in machine-readable format for 90 days post-termination.”

The BATNA reality check

Mutually Assured Compliance Theatre is real. Recorded Future AEs respond to documented competitive POCs, not bluffed alternatives. Authentic leverage requires a parallel evaluation actually in flight, with another vendor’s order form on the table.

In our experience hardening SOC procurement at UnderDefense, the buyers who walk away with the best terms are running a real POC with at least two alternatives, often the UnderDefense Agentic AI SOC platform, CrowdStrike Falcon Intelligence, or Mandiant Advantage. ✅ Without that, the leverage is theatre, and the AE knows it.

I might be wrong on one or two specific clause numbers, but the pattern is consistent across every Recorded Future renewal I have seen in the last 18 months.

Q9. How does the December 2024 Mastercard acquisition affect pricing, governance, and procurement risk?

Mastercard closed its $2.65B acquisition of Recorded Future on December 5, 2024, retaining CEO Christopher Ahlberg and operating Recorded Future as an independent subsidiary. Procurement teams should add four contract clauses: assignment rights tied to material change of control, sub-processor disclosure obligations, payment data isolation language, and an exit-rights audit. The strategic rationale is fraud-intelligence integration into a $9 trillion payments network, which creates new data-handling questions buyers must scrub before signing.

The deal closed in December 2024 at $2.65B, and the integration playbook started rolling out across 2025. By 2026, Mastercard’s threat-intelligence-as-a-service positioning is visible in cross-sell motions, particularly around Payment Fraud Intelligence. Our MDR for Financial Services page covers the parallel risk posture for regulated buyers.

Governance status today

Recorded Future operates as an independent subsidiary, with Christopher Ahlberg retained as CEO. That structure preserves brand continuity, but it does not eliminate the procurement risks created by sitting inside a $9 trillion payments network. I have sat in two GC reviews of Recorded Future renewals since the close, and the same three questions come up every time: assignment, sub-processors, and payment-data isolation.

The four-clause procurement checklist

- Assignment rights tied to material change of control. If Mastercard restructures or divests, your contract should not transfer without your consent.

- Sub-processor disclosure obligations. Demand a written list of sub-processors, with 30-day notice on additions.

- Payment data isolation language. Explicit prohibition on co-mingling your query history with Mastercard payment-network data.

- Exit-rights audit. Right to audit data deletion within 90 days of contract termination.

A General Counsel at a 6,000-person manufacturer told me on a procurement call, “I do not actually care that Mastercard owns them. I care that I cannot trace where my query history flows in 18 months.” That is the honest version of this risk. ❌ Without a written sub-processor disclosure obligation, you are trusting a press release. ✅ With one, you have audit standing if anything shifts.

Compliance overlay

For regulated industries, the Mastercard parent introduces additional questions under PCI DSS, SOC 2, and the EU’s DORA framework. Recorded Future’s existing certifications carry forward, but the data-flow diagram now includes a payments network. Our DORA testing guide covers the operational resilience implications for EU financial entities, and our compliance services page outlines the audit posture buyers should request.

Strategic pricing risk

⚠️ The risk is bundling pressure. Mastercard’s commercial leverage with banks and PSPs means Recorded Future renewals into financial services accounts may carry implicit cross-sell expectations. Buyers in fintech and banking should explicitly confirm pricing is decoupled from any Mastercard product family. For a broader read on switching pressures, our why businesses switch providers piece covers the same dynamic.

In our experience hardening procurement at UnderDefense, ownership change is rarely the actual problem, but the contract clauses written before ownership changes are. ✅ The four-clause checklist above is portable to any post-M&A vendor review, including the next inevitable cybersecurity acquisition.

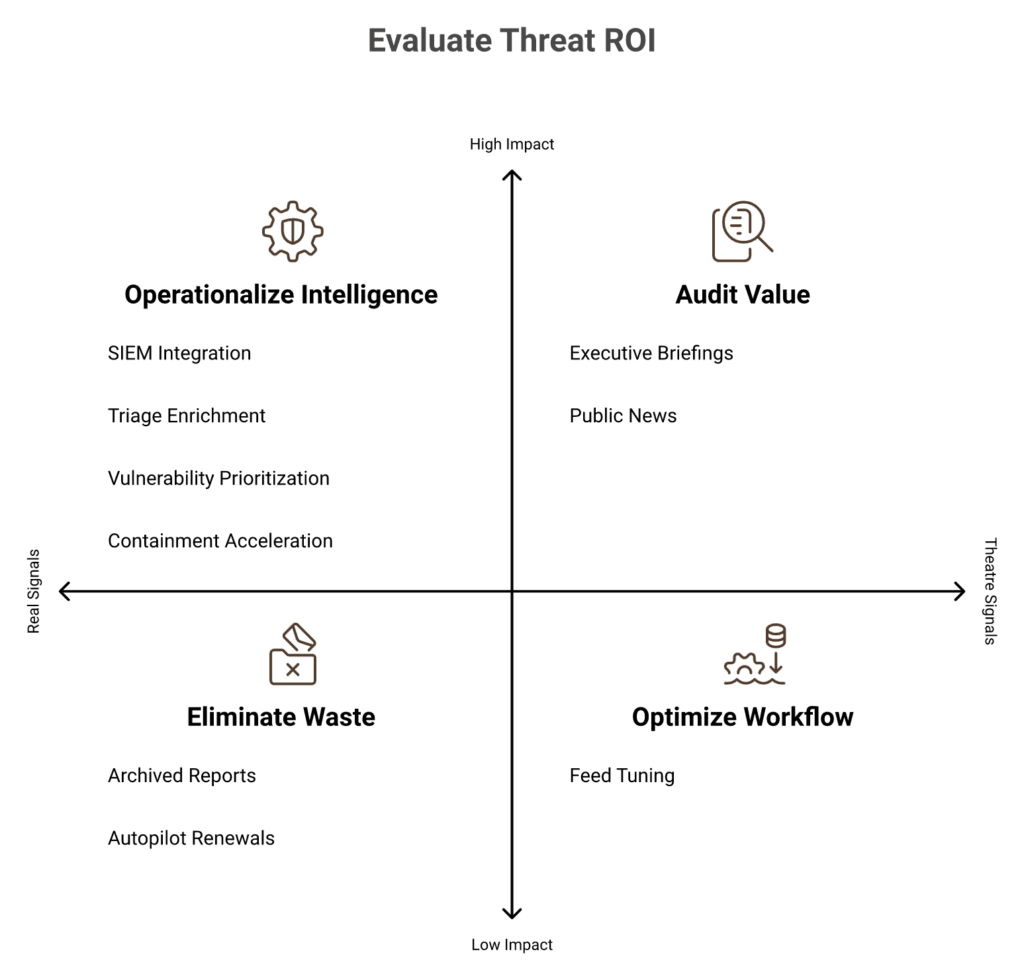

Q10. Is threat intelligence actually worth the spend, or is it expensive news?

Threat intelligence is worth the spend when it produces measurable detection lift, faster triage, or reduced breach impact. Recorded Future cites a 254% three-year ROI in a March 2025 commissioned study, with $19.7M in benefits over three years. The honest counterpoint, USENIX Security 2020 Bouwman et al., found only 1.3% to 4% indicator overlap across paid feeds, meaning most buyers pay premium prices for marginally differentiated data. The ROI is real when the platform feeds detection engineering. The ROI is theatre when reports sit in a SharePoint folder no analyst opens.

The ROI math, both sides

The vendor-funded study is a useful upper bound, and a deeply optimistic one. The USENIX research is a useful floor, because it measured indicator overlap across actual deployments rather than self-reported value. The truth lives between them, and it depends almost entirely on operationalisation discipline. Our SOC metrics (MTTD, MTTR) piece walks through how to measure detection lift honestly.

When TI ROI is real

- Detection engineering team integrates feeds into SIEM correlation rules.

- Tier 1 analysts use enrichment in triage workflows daily.

- Vulnerability prioritisation pulls from intel-driven scoring, not raw CVSS.

- Incident response retros cite specific intel that shortened containment.

When TI ROI is theatre

- Reports are read by a single CTI analyst, then archived.

- Feeds flow to SIEM but never tune detection rules.

- Executive briefings repackage public news with a vendor logo.

- Renewal happens on autopilot without measuring detection lift year-over-year.

The “expensive news” diagnosis

If your TI program produces decks instead of detections, it is expensive news. Working with 500+ security teams, what I have noticed is that the median enterprise underuses the threat intelligence they already pay for. The fix is not buying more, but instrumenting consumption. Our SOC automation playbook outlines the consumption discipline.

The detection lift test

📊 The single test that separates real ROI from theatre: can you name three detections in production today that exist because of your TI feed, and would not exist without it? If the answer is fewer than three, you are paying for news.

“UnderDefense Agentic AI SOC is one of those tools that just clicks for our team. The dashboard is so easy to navigate, even our newer team members can jump in without much training… I will say the integrations took a bit of patience to get right, but their support team was super helpful through it all.”

— Verified User in Computer Software UnderDefense G2 – Verified Review

The Cyber Threat Alliance reality check

The CTA shares adversary playbook intelligence across 34 member vendors at zero marginal cost via STIX. If your EDR or NGFW vendor is in CTA, you are already receiving curated threat intelligence as part of that subscription. Buying a second premium feed on top often duplicates 60% to 80% of the indicators, especially for commodity malware. Our top threat detection tools roundup applies the same overlap test to detection platforms.

The honest ROI framing

In our experience hardening SOCs at UnderDefense, the ROI question is the wrong question. The right question is: what is the marginal detection lift per dollar, after accounting for what you already own? That math kills two to three modules in most quotes, and it strengthens the case for the modules that survive. Our MDR service integrates this discipline into a flat-rate engagement, with detection outcomes tracked monthly.

What my experience of shipping UnderDefense Agentic AI SOC tells me is this: ✅ ROI is highest when threat intelligence feeds an autonomous response loop, not a quarterly board deck. The 2-minute Alert-to-Triage SLA only works because the TI is fused with EDR and identity at ingestion, not bolted on as a report.

“I felt the pricing was a bit on the high side for our budget but the value we got from the support and feature set made up for it… It would help to see more competitive pricing tiers for smaller teams.”

— Verified User in Information Technology and Services Red Canary – G2 Verified Review

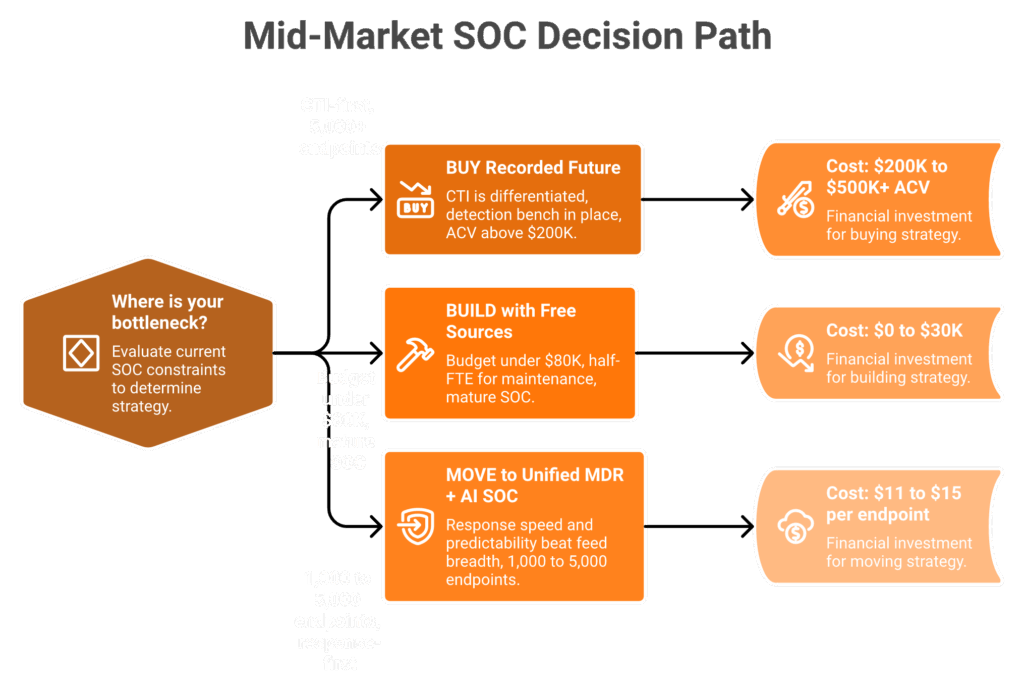

Q11. Should you buy, build, or move? A decision framework for SOC, IR, and CISO buyers.

Buy Recorded Future when CTI is your differentiated capability, you have a detection engineering bench to operationalise feeds, and your budget exceeds $200K ACV with renewal escalation negotiated under 4%. Build using free sources (CISA KEV, MITRE ATT&CK, CTA, MISP, OAuth audits) when budget is under $80K and you have a half-FTE for maintenance. Move to a unified MDR plus AI SOC platform when response speed, alert fatigue, and procurement predictability matter more than feed breadth. Most mid-market buyers (1,000 to 5,000 endpoints) optimise on Move.

The decision matrix

| Path | Best fit | Annual cost | Time to value | Hidden cost |

|---|---|---|---|---|

| Buy (Recorded Future) | CTI-first shop, 5,000+ endpoints | $200K to $500K+ | 3 to 6 months | Detection engineering FTE |

| Build (free sources) | Budget under $80K, mature SOC | $0 to $30K (tooling) | 2 to 4 months | Half-FTE maintenance |

| Move (unified MDR + AI SOC) | 1,000 to 5,000 endpoints, response-first | $11 to $15 per endpoint/mo flat | 2 to 6 weeks | Integration onboarding only |

The Buy path

Choose Buy when CTI is genuinely differentiated for your business. A pure-play threat-intelligence team at a financial-services firm, a defence contractor, or a pharma company with active nation-state exposure earns its keep on Recorded Future or Mandiant. The signal is whether your CTI lead can name three production detections per quarter that exist because of premium feeds. Our MDR buyers guide covers the bench requirements that determine whether Buy is operationally honest.

The Build path

Choose Build when budget is constrained and SOC maturity is already strong. The five free sources (CISA KEV, MITRE ATT&CK enrichment, M365/Google OAuth audits, CTA STIX feeds, MISP) cover roughly 60% to 70% of what entry-tier paid TI delivers, at the cost of a half-FTE in maintenance. Our building a SOC guide covers the staffing pattern that makes Build sustainable.

When Build fails

❌ Build fails when the half-FTE leaves and the institutional knowledge walks with them. ❌ Build also fails when the team mistakes data collection for detection. The MISP instance running unattended is not threat intelligence, but a database.

The Move path

Choose Move when response speed, alert fatigue, and procurement predictability matter more than feed breadth. ✅ Most mid-market buyers (1,000 to 5,000 endpoints) optimise here, because the bottleneck is rarely intel collection, but the gap between detection and action.

UnderDefense Agentic AI SOC delivers a 2-minute Alert-to-Triage SLA with 15-minute escalation for critical incidents, autonomous response actions, and flat-rate $11 to $15 per endpoint per month pricing. The UnderDefense Agentic AI SOC platform ingests threat intelligence alongside EDR, identity, and cloud telemetry, then runs the correlation and response in one place. For the operational pattern, see our MDR reduced MTTR to 9 min case study.

The signal that Move is right

📊 If your team is asking, “Why are we still triaging the same five alert types every shift?” or “Why does our renewal go up 7% every year?”, you are signalling response and predictability problems, not intel-collection problems. Move solves both. Our outsourced vs in-house SOC piece covers the operational trade-offs.

The contrarian close

I might be wrong on the exact percentage, but the pattern is consistent. The majority of mid-market buyers I talk to are running a Buy strategy because they bought it three years ago, not because they audited the alternatives in the last 12 months. The audit takes one analyst week. The savings, on average, fund a full year of MDR coverage.

“Reliable Cybersecurity Partner with Stellar Service… UnderDefense doesn’t just deliver products, they deliver outcomes. Their team feels like an extension of ours.”

— Verified User in Computer & Network Security UnderDefense G2 – Verified Review

Less theatre, more throughput. Less black box, more blue team. ✅ If you want to see the math against your specific environment, our book a demo page is the fastest path to a side-by-side comparison.

Turn these benchmarks into a real plan.

Get a vendor-neutral assessment and a cost-optimized roadmap.

References

Research Papers

- Bouwman, X., Griffioen, H., Egbers, J., Doerr, C., Klievink, B., van Eeten, M. “A Different Cup of TI? The Added Value of Commercial Threat Intelligence.” USENIX Security Symposium, 2020.

Official Docs / Indian Statutes

- SEC. “Cybersecurity Risk Management, Strategy, Governance, and Incident Disclosure (Form 8-K Item 1.05).” Published: July 2023.

- EU. “GDPR Article 33: Notification of a Personal Data Breach to the Supervisory Authority.” Regulation (EU) 2016/679.

- EU. “NIS2 Directive (EU) 2022/2555.” Published: December 2022.

- NIST. “SP 800-61 Rev. 2: Computer Security Incident Handling Guide.” Published: 2012.

- CISA. “Known Exploited Vulnerabilities Catalog.” Cybersecurity and Infrastructure Security Agency.

Datasets

- Vendr Marketplace. “Recorded Future Software Pricing & Plans 2026,” 2026.

Blogs

- Recorded Future. “A New Way to Buy Recorded Future: Solutions and Packages Built for the 2026 Threat Landscape.” Published: April 13, 2026. [Secondary source]

- Recorded Future. “Mastercard Invests in Continued Defense of Global Digital Economy.” Published: September 11, 2024. [Secondary source]

- Mastercard. “Mastercard Finalizes Acquisition of Recorded Future.” Published: December 19, 2024. [Secondary source]

- Recorded Future. “How Recorded Future Boosts Cybersecurity ROI & Efficiency.” Published: March 26, 2025. [Secondary source]

- Forrester Consulting. “The Total Economic Impact of Recorded Future Intelligence Platform.” [Secondary source]

- Reuters / Yahoo Finance. “Mastercard bolsters threat intelligence capabilities with $2.65 billion deal for Recorded Future.” Published: September 12, 2024. [Secondary source]

- IBM. “Cost of a Data Breach Report 2025.” [Secondary source]

- Recorded Future. “Predictable Pricing.” [Secondary source]

- Recorded Future. “Compare Threat Intelligence Packages, License Options.” [Secondary source]

- Recorded Future. “2026 Pricing PDF.” [Secondary source]

- UnderDefense Agentic AI SOC. “G2 Verified Reviews.” [Secondary source]

- Arctic Wolf, Red Canary, Rapid7, Alert Logic, Expel. “G2 and Gartner Verified Reviews.” [Secondary source]

1. How much does Recorded Future cost in 2026, and why is pricing not published?

In our experience guiding mid-market and enterprise buyers, Recorded Future stays quote-only because the bundled-quote model preserves their commercial leverage. Verified Vendr transaction data we benchmark against shows entry contracts start at $40,000 to $60,000 for a single module, mid-market deployments land between $75,000 and $200,000 ACV across three to five modules, and full-suite enterprise contracts run $250,000 to $500,000+. Pricing is shaped by four levers, in this order: package selection (Core, Professional, or Elite), organisation size, usage volume (API calls and Intelligence Graph enrichment), and services tier including Insikt Group hours. The 2026 unlimited-user model sounds generous, but the meter just shifted from seats to API calls. We have watched mid-market teams burn their query allotment by week three of a quarter, then face renewal uplifts that look suspiciously like the original quote plus 22%. For a transparent flat-rate alternative, we publish our own MDR pricing at $11 to $15 per endpoint per month, no per-API-call surprises.

2. What is the difference between Recorded Future Core, Professional, and Elite?

All three packages ride the same Intelligence Graph (1.2M sources, 26B entities) with unlimited users and integrations.

-

Core: Cyber Operations and Digital Risk Protection. Suits a 1,000 to 2,000-person SaaS with a small SOC focused on triage enrichment and brand monitoring.

-

Professional: Adds Attack Surface Intelligence and Autonomous Threat Hunting. Fits teams without a mature detection-engineering bench.

-

Elite: Adds Third-Party Risk for full cross-domain coverage. Earns its keep at 5,000+ employees with global supply-chain exposure.

Payment Fraud Intelligence remains a standalone add-on for financial institutions. In our experience hardening SOCs at UnderDefense, the integration into your SIEM detection pipeline eats roughly 40% of the Year 1 value of any tier upgrade. Our guide to MDR services covers the operationalisation discipline that makes premium tiers worth the spend.

3. What hidden fees and add-ons should we negotiate before signing?

Seven hidden costs consistently ambush buyers:

-

API overages with no published cap ($5K to $25K per quarter in surprise charges).

-

Premium Success TAM at 10% to 20% of base ACV ($20K to $80K per year).

-

Insikt Group custom research at $50K to $150K per project.

-

Custom SIEM/SOAR integration professional services at $15K to $40K per integration.

-

Advanced training capped at 15 seats per year.

-

Renewal escalation defaulting to 5% to 7% annually.

-

Dark-web data purchases scoped as discrete add-ons.

Vendr data shows scope-confirmation before signing avoids $15K to $75K in unexpected costs. The non-negotiable clauses we recommend: cap API overage at 10% of base ACV, bundle TAM into base for any deal above $200K ACV, and cap renewal escalation at 3%. Our MDR buyers guide walks through the same trap on the MDR side, with the exact clause language to scrub.

4. What is the realistic 3-year TCO for Recorded Future at different organisation sizes?

Modelling against Vendr Marketplace 2026 transaction data with a 3% negotiated escalation cap, 15% Premium Success TAM uplift, 5% API buffer in Years 2 and 3, and one-time Year 1 onboarding:

-

50-analyst Core deployment: approximately $458K over three years ($3,053 per seat per year blended).

-

200-analyst Professional deployment: approximately $1.13M ($1,883 per seat per year).

-

500-analyst Elite deployment: approximately $2.24M ($1,493 per seat per year).

The hidden delta is escalation. On a $300K starting ACV, the Year 3 cost difference between 3% and 7% escalation is $25.2K, and the cumulative 3-year delta is $63K. On a $600K Elite contract, the delta balloons to $126K. For a like-for-like flat-rate model, our SOC cost calculator and cybersecurity budget 2026 playbook show how to defend the escalation cap to a CFO.

5. How does Recorded Future compare to UnderDefense Agentic AI SOC, Mandiant, and CrowdStrike Falcon Intelligence?

UnderDefense Agentic AI SOC flips the model from “data feed” to unified AI SOC plus Human Ally on flat-rate pricing ($11 to $15 per endpoint per month) with 2-minute Alert-to-Triage and autonomous response. Recorded Future ($50K to $500K+) and Mandiant Advantage ($50K to $600K) sit in the same premium-feed tier. CrowdStrike Falcon Intelligence ($15 to $40 per endpoint) wins if you are already on Falcon EDR. The bottleneck for most mid-market buyers is rarely “more data,” but the gap between detection and action. Recorded Future tells you what is out there, then hands you a Slack-style alert and walks away. The UnderDefense Agentic AI SOC platform ingests threat intelligence alongside EDR, identity, and cloud telemetry, then runs the correlation and response in one place. Our CrowdStrike vs SentinelOne breakdown applies the same outcome-per-dollar lens.

6. What free or already-owned alternatives should we audit before buying Recorded Future?

Before purchasing, we recommend auditing five free or already-owned sources:

-

CISA Known Exploited Vulnerabilities (KEV) Catalog: substitutes 60% of Vulnerability Intelligence triage logic.

-

MITRE ATT&CK enrichment: free in most modern SIEMs in 2026.

-

M365 / Google OAuth consent log audits: surface Shadow IT in place of Attack Surface Intelligence.

-

Cyber Threat Alliance (CTA) STIX feeds: shared adversary playbook intelligence across 34 member vendors at zero cost.

-

MISP (Malware Information Sharing Platform): community IOC sharing.

USENIX Security 2020 (Bouwman et al.) measured only 1.3% to 4% indicator overlap across paid commercial feeds, meaning two vendors selling premium TI to the same buyer agree on a few percent of what matters. This audit takes one analyst week and routinely strips two to three modules out of the quote. Our security stack guide covers the same audit discipline applied across the full security stack.

7. How does the Mastercard acquisition affect Recorded Future contracts and procurement risk?

Mastercard closed its $2.65B acquisition of Recorded Future on December 5, 2024, retaining CEO Christopher Ahlberg and operating Recorded Future as an independent subsidiary. Procurement teams should add four contract clauses:

-

Assignment rights tied to material change of control.

-

Sub-processor disclosure obligations with 30-day notice on additions.

-

Payment data isolation language preventing co-mingling with Mastercard payments-network data.

-

Exit-rights audit, with right to verify data deletion within 90 days of termination.

For regulated industries, the Mastercard parent introduces additional questions under PCI DSS, SOC 2, and DORA. Existing certifications carry forward, but the data-flow diagram now includes a payments network. Buyers in fintech and banking should explicitly confirm pricing is decoupled from any Mastercard product family. Our DORA testing guide and compliance services page outline the audit posture buyers should request.

8. Should we buy Recorded Future, build with free sources, or move to a unified MDR platform?

We frame the decision in three paths:

-

Buy Recorded Future when CTI is your differentiated capability, you have a detection-engineering bench, and your budget exceeds $200K ACV with renewal escalation negotiated under 4%.

-

Build using free sources (CISA KEV, MITRE ATT&CK, CTA, MISP, OAuth audits) when budget is under $80K and you have a half-FTE for maintenance.

-

Move to a unified MDR plus AI SOC platform when response speed, alert fatigue, and procurement predictability matter more than feed breadth.

Most mid-market buyers (1,000 to 5,000 endpoints) optimise on Move. The single test that separates real ROI from theatre: can you name three detections in production today that exist because of your TI feed? If fewer than three, you are paying for news. See our outsourced vs in-house SOC framework for the operational trade-offs, and book a demo for a side-by-side comparison against your environment.