Q1. What Is Data Governance in Financial Services and Why Does It Matter in 2026?

Data governance in financial services is the system of policies, roles, standards, metrics, and technologies that ensures financial data is accurate, secure, traceable, and compliant throughout its entire lifecycle. It spans every asset from customer PII to AI model outputs, and it answers one question every regulator will eventually ask: Can you prove your data is trustworthy?

Governance vs. Management: A Critical Distinction

These terms get used interchangeably, and that confusion causes real problems when you’re sitting across from an examiner. Here’s the clean split:

| Dimension | Data Governance | Data Management |

|---|---|---|

| Scope | Sets rules, accountability, and decision rights | Executes operational processes on data |

| Ownership | CDO, governance council, data stewards | Data engineers, DBAs, ETL developers |

| Output | Policies, standards, metrics, compliance evidence | Clean pipelines, stored data, reports |

Governance tells you who can do what with data and why. Management does the work. Without governance, management is just busy work with no audit trail.

Seven Data Types Financial Institutions Must Govern

Not all data carries equal risk, and not all of it sits where you think it does:

- Customer / PII Data, names, SSNs, account details. The obvious one, and the one regulators check first.

- Transactional Data, payments, trades, transfers. Drives real-time fraud detection and regulatory reporting.

- Market & Reference Data, pricing, benchmarks, counterparty identifiers. Bad reference data means bad risk calculations, full stop.

- Regulatory & Compliance Data, audit logs, SAR filings, capital adequacy reports. Must be lineage-complete and immutable.

- Communications & Off-Channel Data, emails, Slack messages, WhatsApp threads. The SEC has levied over $3 billion in fines since 2021 for firms failing to capture these.

- AI-Derived & Model Output Data, credit scores, fraud predictions, algorithmic trading signals. If you can’t govern the input, you can’t trust the output.

- Third-Party & Shadow Data, vendor feeds, ungoverned copies sitting in departmental spreadsheets and personal drives. Shadow data is often the root cause of audit findings and breaches.

Data Classification by Risk Level

| Risk Level | Examples | Governance Priority |

|---|---|---|

| ⚠️ Regulated | PII, payment card data, health records | Mandatory controls, encryption, full lineage |

| ✅ Operational | Transactional, market, reference data | Quality gates, access controls, retention policies |

| Low-Sensitivity | Aggregated analytics, anonymized datasets | Standard classification, periodic review |

| ❌ Shadow | Untracked copies, personal device exports | Discovery, remediation, or deletion |

Six Core Principles

- Accountability, every data asset has a named owner responsible for its quality and compliance.

- Transparency, policies, lineage, and access decisions are documented and auditable.

- Data Quality, automated validation ensures accuracy, completeness, and timeliness at the source.

- Regulatory Compliance, controls map directly to specific regulatory requirements, not generic checkboxes.

- Standardization, enterprise-wide definitions, formats, and taxonomies eliminate ambiguity across business lines.

- Cross-Functional Collaboration, governance is not an IT project. It requires business, risk, compliance, and technology working from the same playbook.

Why 2026 Is the Inflection Point

Multiple regulatory timelines are converging simultaneously. DORA is now in enforcement, with only 50% of financial institutions estimated to be fully compliant and fines reaching up to 10% of annual turnover. The EU AI Act classifies financial AI systems (credit scoring, fraud detection, insurance pricing) as high-risk, requiring governed training data and explainability audits. GDPR enforcement continues to intensify, Basel III Endgame implementation is reshaping capital adequacy data requirements, and cross-border data sovereignty mandates from India’s DPDPA to China’s PIPL are adding new layers of complexity.

Meanwhile, digital transformation has expanded the average financial institution’s data estate faster than governance programs can scale. The result: more data, more regulation, less visibility, exactly the combination that produces audit findings, breaches, and penalties. For institutions navigating these overlapping mandates, a compliance roadmap that maps governance controls to specific regulations is no longer optional.

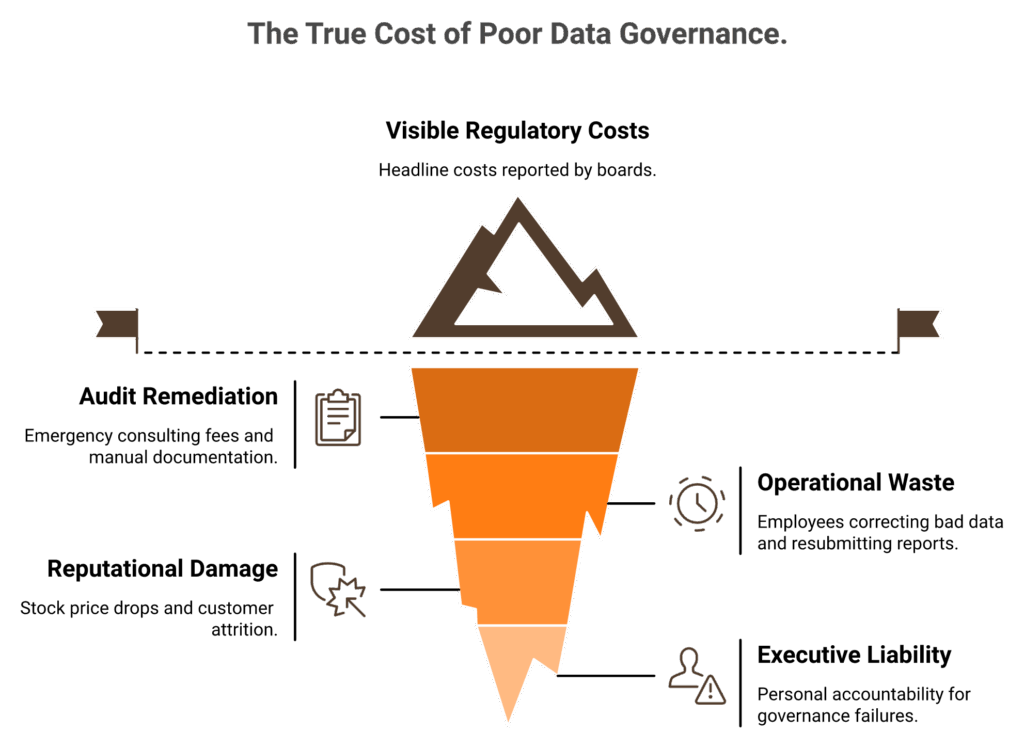

Q2. What Is the Real Cost of Poor Data Governance in Financial Services?

Picture this: a compliance officer at a mid-tier bank receives notice of a regulatory examination in 30 days. Examiners want full data lineage for three critical regulatory reports. The bank’s governance program covers 40% of data assets. The CDO scrambles to produce documentation manually: 400+ person-hours, $200K in emergency consulting fees, and a Matters Requiring Attention finding that triggers board-level scrutiny.

This pattern repeats across financial services because governance was treated as a “someday” initiative until the examiner showed up.

The Numbers Behind the Damage

Gartner estimates poor data quality costs organizations an average of $12.9–$15 million per year. In financial services, where data drives every risk decision, regulatory filing, and customer interaction, the impact compounds fast.

| 💸 Cost Category | Benchmark |

|---|---|

| Regulatory Penalties | GDPR: single fines up to €1.2B; SEC off-channel: $3B+ cumulative since 2021 |

| Breach Response | Financial services breaches rank among the costliest across industries (IBM) |

| Audit Remediation | 200+ person-hours per exam for manual lineage documentation |

| Operational Waste | Employees spend up to 27% of their time correcting bad data |

| Reputational Damage | Stock price drops, customer attrition, board-level consequences |

❌ Real-World Governance Failures

These are not edge cases. They are the consequences of governance gaps at scale:

- Equifax (2017): 143 million records exposed. Root cause: failure to patch a known vulnerability and absence of network segmentation, basic governance failures. Settlement: up to $700 million.

- Capital One (2019): 106 million customer records exposed via a misconfigured cloud firewall. The OCC fined Capital One $80 million specifically for “failure to establish effective risk assessment processes prior to migrating IT operations to the public cloud.”

- Danske Bank (2007–2015): €200 billion in suspicious transactions flowed through the Estonian branch. Data governance gaps enabled AML blind spots across years of operations. The CEO resigned, ten employees were arrested, and Denmark increased money-laundering penalties eightfold.

- SEC Off-Channel Enforcement (2021–2024): Over $3 billion in cumulative fines against 100+ financial firms for failing to capture and archive business communications on WhatsApp, personal devices, and unauthorized platforms. In 2024 alone, the SEC imposed over $600 million in penalties against more than 70 firms.

These failures underscore why continuous security monitoring and governance enforcement must work in tandem, not as separate initiatives.

⚠️ Personal Executive Liability

This is the part that should keep CDOs and CISOs up at night. The UK’s Senior Managers & Certification Regime (SM&CR) holds individual executives personally accountable for governance failures within their scope of responsibility. The institution does not face consequences alone; the named individual on the accountability map faces them as well.

The US is trending in the same direction. The SEC’s enforcement actions increasingly name senior managers who failed to supervise compliance with recordkeeping obligations. When a governance breakdown happens on your watch, the question is not just “what did the firm know?” but rather “what did you do about it?”

Governance is no longer just an institutional risk sitting in a compliance slide deck. It is a personal, career-defining one. That’s the real cost, and it’s the reason “we’ll get to it next quarter” is no longer an acceptable answer. For leaders looking to quantify this risk for their board, a cybersecurity budget playbook can help frame governance investment as revenue protection.

Q3. Which Regulations Drive Data Governance Requirements Across Financial Services?

Financial institutions in 2026 don’t face regulations one at a time. They face overlapping mandates across data quality, privacy, operational resilience, financial reporting, transaction transparency, payment security, AI accountability, cybersecurity, and recordkeeping. The challenge is not understanding any single regulation; it’s managing the convergence.

Regulatory Comparison Matrix

| Regulation | Jurisdiction | Primary Governance Requirement | Key Dimensions | Enforcement 2026 | Penalty Range |

|---|---|---|---|---|---|

| BCBS 239 | Global (Basel) | Risk data aggregation accuracy, completeness, timeliness | Lineage, Quality | Active supervisory reviews | Supervisory action, MRAs |

| Basel III / Endgame | Global / US | Capital adequacy data integrity for stress testing | Quality, Access | Phased implementation | Capital surcharges |

| GDPR | EU/EEA | Data protection, consent management, right to erasure | Access, Retention, Classification | Active enforcement | Up to 4% global revenue or €20M |

| GLBA | US | Safeguarding customer financial information | Access, Quality | Active | Fines + personal liability |

| SOX | US | Financial reporting data integrity and internal controls | Lineage, Quality | Active | Up to $5M + imprisonment |

| Dodd-Frank / OFR | US | Systemic risk data lineage and reporting | Lineage, Quality | Active | Varies by violation |

| PCI-DSS 4.0 | Global | Payment card data security standards | Access, Classification | Required compliance | Fines + loss of processing rights |

| MiFID II | EU | Transaction reporting, data transparency | Lineage, Retention | Active | Varies by member state |

| DORA | EU | ICT risk management, data integrity during disruptions | Lineage, Quality, Access | In force since Jan 2025 | Up to 10% annual turnover |

| EU AI Act | EU | High-risk AI governance, training data documentation | Classification, Quality, Lineage | Phased 2024–2026 | Up to €35M or 7% revenue |

| 23 NYCRR 500 | US (NY) | Cybersecurity program, data encryption, access controls | Access, Classification | Active (amended 2023) | Per-violation penalties |

| SEC Rule 204-2 | US | Recordkeeping, communication retention | Retention | Active | $3B+ cumulative since 2021 |

| FinCEN | US | AML/KYC data reporting, suspicious activity monitoring | Quality, Retention | Active | Per-violation + criminal |

| CPRA | US (CA) | Consumer data rights, privacy controls | Access, Retention, Classification | Active | $7,500 per intentional violation |

⏰ DORA and EU AI Act: The 2026-Critical Regulations

DORA (Digital Operational Resilience Act) went into enforcement in January 2025, and national regulators are now actively reviewing compliance. The requirements that hit data governance hardest:

- Maintain data integrity and availability during ICT disruptions

- Report major ICT incidents to regulators within 4 hours of classification

- Conduct third-party ICT risk governance, including mandatory contract clauses covering data processing locations, exit strategies, and audit rights

- Significant entities must perform Threat-Led Penetration Testing (TLPT) at least every three years

Only 50% of financial institutions are estimated to be fully DORA-compliant, meaning half the industry is operating with enforcement risk right now. For institutions preparing for DORA penetration testing requirements, the timeline to close compliance gaps is shrinking fast.

EU AI Act classifies credit scoring, fraud detection, and insurance pricing AI as “high-risk” systems. This means:

- Training data must be governed, documented, and bias-tested

- Model explainability audits are mandatory

- Human oversight mechanisms must be in place

- Post-deployment monitoring for drift and fairness is required

For institutions already struggling with basic data lineage, layering AI governance requirements on top creates a compounding challenge.

🌍 Cross-Border Data Sovereignty

Global banks face conflicting data residency demands across jurisdictions. EU GDPR restricts data transfers outside the EEA. The US CLOUD Act enables extraterritorial access. India’s DPDPA imposes localization requirements for certain data categories. China’s PIPL requires critical information infrastructure operators to store data domestically.

Practical resolution requires three things:

- Jurisdiction-aware policy engines that apply the correct controls based on where data resides and flows

- Data residency tagging in catalogs so every asset carries its jurisdictional classification

- Sovereign cloud deployment strategies that satisfy local requirements without fragmenting the global governance framework

The institutions that treat regulations as individual compliance projects will always be scrambling. The ones that build governance frameworks addressing regulatory intersections, where data lineage satisfies BCBS 239, GDPR right-to-explanation, and EU AI Act explainability simultaneously, reduce duplication and audit burden by design.

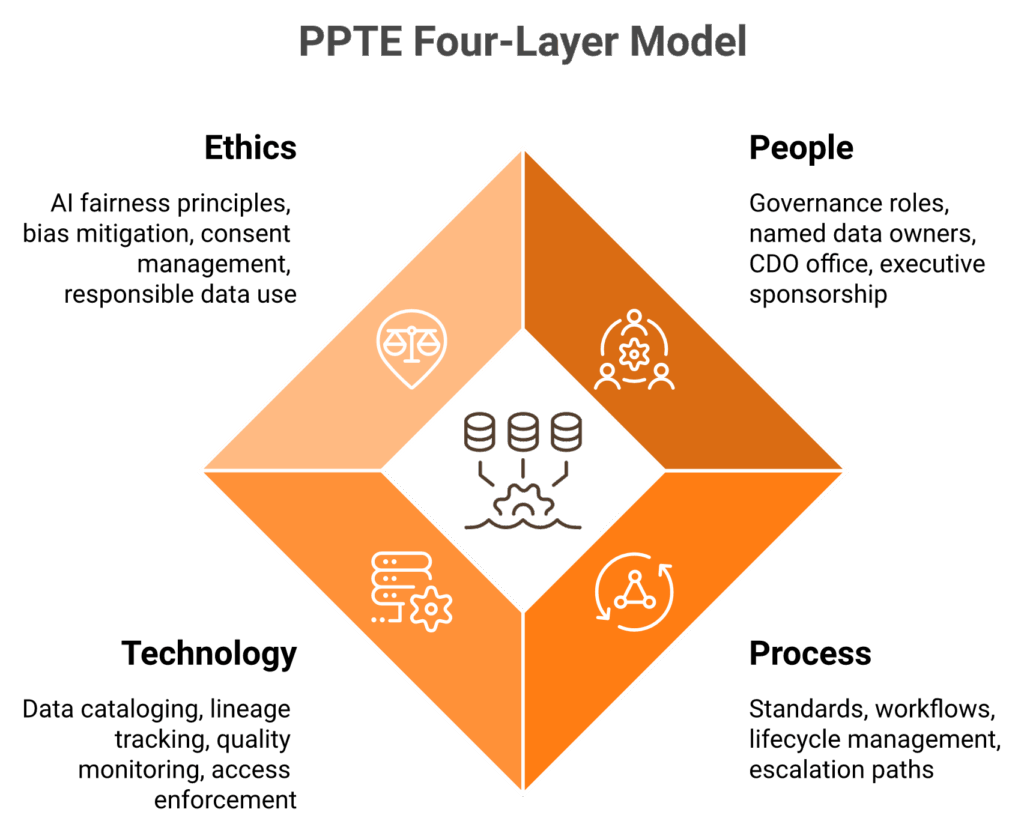

Q4. What Are the Core Components of a Scalable Data Governance Framework?

Most governance frameworks fail not because the technology is wrong, but because an entire layer is missing. From what I’ve seen across financial institutions of every size, the ones that succeed think in four layers, not one.

The PPTE Four-Layer Model

- People, governance roles, accountability structures, executive sponsorship. Without named owners, policies are orphans.

- Process, standards, workflows, lifecycle management, escalation paths. The operational muscle that turns policy into practice.

- Technology, platforms for cataloging, lineage, quality monitoring, access enforcement, and automation. The accelerator, but never the foundation.

- Ethics, data ethics principles governing AI fairness, bias mitigation, consent management, and responsible use. This is the layer most financial institutions skip, and it’s exactly where regulators are heading next.

Scalable frameworks require all four. Most governance failures trace directly back to missing People or Ethics, the two layers you can’t buy off a vendor’s product page.

Six Core Framework Pillars

| # | Pillar | Purpose | Key Deliverable | Primary Regulation Served |

|---|---|---|---|---|

| 1 | Data Catalog & Discovery | Enterprise-wide inventory with business context and automated discovery | Searchable asset registry with owners, definitions, classifications | BCBS 239, GDPR, DORA |

| 2 | Data Quality Management | Profiling, validation rules, automated remediation, quality scoring | Quality dashboards with threshold alerting | BCBS 239, SOX, Basel III |

| 3 | Metadata Management | Technical and business metadata linking data to policies and lineage | Unified metadata repository connecting governance to operations | EU AI Act, MiFID II |

| 4 | Data Lineage | End-to-end traceability from origination through transformation to report | Visual lineage maps for every regulatory report and AI training dataset | BCBS 239, DORA, SOX, EU AI Act |

| 5 | Access Controls & Security | RBAC, zero-trust architecture, encryption, masking, continuous monitoring | Enforced access policies with audit logs | GLBA, PCI-DSS, 23 NYCRR 500, GDPR |

| 6 | Policy Automation | Automated enforcement of classification, retention, disposal, lifecycle rules | Self-executing policies that reduce manual governance overhead | GDPR, SEC Rule 204-2, CPRA |

Governance Roles and Organizational Structure

| Role | Responsibility | Decision Authority |

|---|---|---|

| Chief Data Officer (CDO) | Enterprise data strategy, standards, governance program oversight | Accountable for governance outcomes |

| Data Protection Officer (DPO) | Privacy compliance, GDPR/DPDPA obligations, evolving rapidly in the AI era as model governance intersects privacy | Advisory + compliance authority |

| Data Stewards | Domain-level policy execution, quality monitoring, issue resolution | Responsible for domain data quality |

| Governance Council | Cross-functional oversight, policy approval, priority setting | Consulted on major governance decisions |

| Governance Committee | Executive sponsorship, budget allocation, strategic alignment | Informed of governance program status |

✅ RACI Matrix Template

| Activity | CDO | DPO | Stewards | Council | IT/Engineering |

|---|---|---|---|---|---|

| Policy Creation | A | C | R | C | I |

| Quality Monitoring | A | I | R | I | R |

| Access Reviews | C | R | R | I | A |

| Incident Response | C | R | I | I | A |

| Audit Preparation | A | R | R | C | R |

R = Responsible, A = Accountable, C = Consulted, I = Informed

Federated vs. Centralized: The Hybrid Reality

Most financial institutions in 2026 operate a hybrid federated model: central policy authority sets enterprise-wide standards, and domain-level working groups execute within their areas. Pure centralization is too slow for operational reality. Pure decentralization produces inconsistency that auditors flag immediately. The hybrid approach gives you regulatory consistency where it matters and operational agility where speed matters.

Often-Overlooked Components

Three framework elements get consistently underinvested:

- Enterprise business glossary, if “customer” means something different across retail, commercial, and investment banking, your governance framework is already broken. Standardized terms and metrics are the foundation of cross-department data consistency.

- Data retention and disposal policies, GDPR says delete; SEC says retain for seven years. These mandates directly conflict. Resolution requires purpose-based retention with documented legal basis for every data category.

- Data contracts, formal agreements governing data exchange between internal domains and external partners/APIs. As open banking and embedded finance expand, data contracts become the governance mechanism for data flowing across organizational boundaries. Organizations looking to formalize these controls can benefit from a virtual CISO who brings cross-industry governance expertise without a full-time hire.

Q5. How Do Banks, Fintechs, Insurers, and Asset Managers Approach Data Governance Differently?

Governance requirements vary dramatically across financial sub-verticals based on regulatory exposure, data types, technology maturity, and operational models. A global bank running 30-year-old core banking systems faces fundamentally different governance challenges than a three-year-old neobank running entirely on APIs and cloud-native microservices.

The Sub-Vertical Governance Landscape

| Dimension | Traditional Banks | Fintechs / Neobanks | Insurers | Asset Managers |

|---|---|---|---|---|

| Governance Model | Centralized, hierarchical, committee-driven | Agile, embedded in CI/CD, policy-as-code | Actuarial-centric, claims-driven | Front-office / back-office split |

| Primary Regulations | Basel III, BCBS 239, GLBA, SOX, DORA | PSD2/PSD3, evolving fintech mandates, GDPR | Solvency II, IFRS 17, state-level mandates | MiFID II, AIFMD, SEC Rule 204-2 |

| Key Data Types | Core banking, payment, KYC/AML | Real-time transactional, API telemetry, behavioral | Actuarial, claims, underwriting, policyholder PII | Portfolio, market/reference, NAV, backtesting |

| Technology Stack | On-prem legacy + modernization layers | Cloud-native, data mesh, event-driven | Hybrid (legacy mainframe + digital front-end) | Specialized platforms (Bloomberg, Aladdin) |

| Top Challenge | Legacy modernization without breaking lineage | Scaling governance with hypergrowth | Data quality across long-tail policy portfolios | Backtesting integrity and alpha-generation data |

Cross-Cutting Governance Concerns

Three themes now span every sub-vertical, and the institutions handling them well are the ones that built governance into their architecture rather than bolting it on after the fact.

Open Banking & PSD2/PSD3: The EU’s PSD3 framework strengthens API security requirements, mandates explicit consent verification for all data-sharing actions, and requires auditable logs for every access request. For banks, this means governing third-party data access at the API layer: who is pulling what data, under what consent, and with what audit trail. For fintechs acting as third-party providers (TPPs), it means demonstrating governance maturity to banking partners who are increasingly demanding it.

Embedded Finance / BaaS: Banking-as-a-Service providers govern data flowing through API ecosystems to non-financial partners. When a retailer offers financing through a BaaS API, the governance question becomes: who owns the data, who governs it, and which regulatory framework applies? The answer is usually “all of them simultaneously.” Institutions running cloud security across these distributed architectures need governance controls embedded at every integration point.

ESG Data Governance: SFDR and CSRD create overlapping sustainability reporting obligations. Financial market participants must disclose principal adverse impact indicators, while CSRD demands entity-level sustainability reporting with external audit assurance. The core governance problem: ESG data quality is inconsistent, third-party ESG ratings diverge significantly across providers, and there are no universally standardized ESG taxonomies yet.

⏰ The Convergence Trend

Here’s what’s actually happening on the ground: as fintechs mature and acquire banking licenses, their governance requirements converge with traditional bank standards. Banks are adopting fintech practices, including data contracts, API governance, and automated policy enforcement. Insurers are moving from batch-based actuarial processes to real-time underwriting powered by ML models that demand the same model governance rigor as banks. Asset managers are deploying AI-driven analytics for alpha generation, which brings EU AI Act high-risk classification into their governance scope.

The endgame is clear: governance frameworks must be technology-agnostic and sub-vertical-adaptable. An institution that builds governance around a single regulatory mandate or a single technology stack will rebuild it every time the landscape shifts. In 2026, the landscape shifts quarterly. For insurers and financial firms navigating this convergence, a governance framework that adapts across sub-verticals is no longer a luxury but a survival requirement.

Q6. How Do You Build an Audit-Ready Data Governance Framework Step by Step?

Use this 8-step framework to build a governance program that satisfies regulators, passes audits on first review, and scales with institutional growth. Every step maps directly to the audit evidence it produces, because governance that can’t be demonstrated to an examiner doesn’t count.

The 8-Step Implementation Roadmap

- Define governance objectives, scope, and success metrics: Tie them to business outcomes (reduced audit findings, faster regulatory reporting, lower breach exposure), not abstract compliance checkboxes.

- Secure executive buy-in: Frame governance as revenue protection. Lead with the numbers: Gartner’s $12.9–$15M annual cost of poor data quality, $3B+ in SEC off-channel fines since 2021, and the personal liability implications under SM&CR.

- Conduct data landscape assessment: Inventory all data assets across on-prem, cloud, SaaS, and shadow IT. You can’t govern what you can’t find.

- Prioritize Critical Data Elements (CDEs): Start with regulatory-critical data (KYC/AML, financial reporting, payment), then expand iteratively. Trying to govern everything on day one is how programs stall.

- Establish CDO office, governance council, and RACI-mapped stewardship roles: Assign named accountability for every CDE.

- Build governance policies, business glossary, and SOPs: Standardize definitions and workflows enterprise-wide.

- Select and deploy governance technology: Catalog, lineage, quality, and access control platforms that integrate with your existing stack.

- Implement continuous monitoring, training, and refinement cycles: Build a data-literate culture through ongoing education and feedback loops.

Audit Evidence Mapping

| Step | Audit Evidence Produced | Regulation Satisfied |

|---|---|---|

| Step 1 | Documented governance charter with measurable KPIs | BCBS 239, DORA |

| Step 3 | Complete data asset inventory with classification | GDPR, CPRA, PCI-DSS |

| Step 4 | CDE registry with business definitions, owners, and regulatory mapping | BCBS 239, SOX |

| Step 5 | RACI matrix and governance council meeting minutes | GLBA, 23 NYCRR 500 |

| Step 7 | Automated lineage documentation and traceability maps | DORA, SOX, EU AI Act |

| Step 8 | Continuous quality dashboards with threshold alerting | BCBS 239, Basel III |

✅ Audit-Readiness Checklist

- ☐ All CDEs cataloged with business definitions, data owners, and regulatory mapping

- ☐ End-to-end lineage documented for all regulatory reports and AI model training datasets

- ☐ Access control policies mapped to specific regulations with automated enforcement

- ☐ Data quality metrics tracked with automated alerting on threshold breaches

- ☐ Retention and disposition policies automated and auditable across jurisdictions

- ☐ Governance council meeting minutes and decision logs maintained

- ☐ Continuous security monitoring active on all governed data assets with incident response documented

- ☐ Training completion records and data literacy assessments documented for all data stewards

Score Interpretation

| ✅ Checked | Status | Action |

|---|---|---|

| 7–8 | Audit-ready | Focus on optimization and predictive governance |

| 4–6 | ⚠️ Critical gaps | Gaps will surface during examination; prioritize automation and monitoring |

| 0–3 | ❌ Significant remediation | Establish CDO function, engage governance technology vendors before next audit cycle |

Institutions scoring below 5 should prioritize automated governance platforms and continuous security monitoring to close gaps before the next examination window. The cost of manual remediation after an examiner identifies deficiencies is 3–5x higher than proactive implementation.

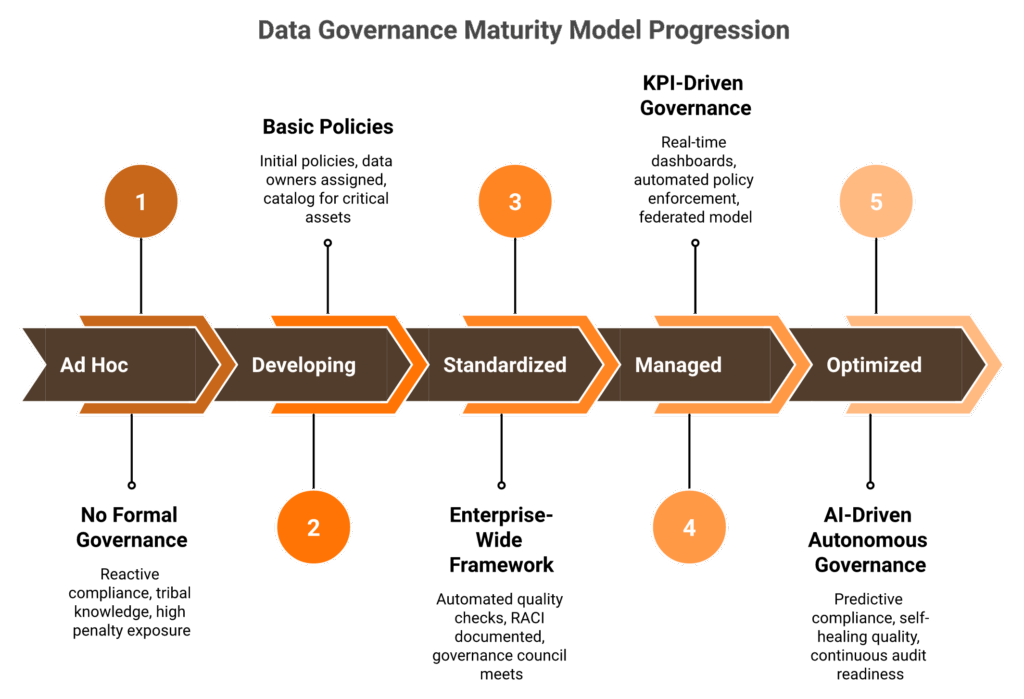

Q7. What Does a Data Governance Maturity Model Look Like for Financial Institutions?

Regulators increasingly expect documented governance maturity progression, not just a static framework, but evidence that you’re advancing. The two industry-standard references are DCAM (Data Management Capability Assessment Model), developed by the EDM Council specifically for financial services, and DAMA-DMBOK for broader data management context. Most financial institutions in 2026 operate at Level 2–3, and the jump from Level 3 to Level 4 is where AI-driven automation becomes critical.

5-Level Maturity Model

| Level | Name | Description | Key Indicator | Risk Exposure |

|---|---|---|---|---|

| 1 | Ad Hoc / Initial | No formal governance, reactive compliance, tribal knowledge, no audit trail | Data quality is “someone else’s problem” | ❌ High penalty exposure |

| 2 | Developing | Basic policies defined, data owners assigned, initial catalog for critical assets, manual quality checks | Catalog covers <40% of CDEs | ⚠️ Audit findings likely |

| 3 | Standardized | Enterprise-wide framework operational, automated quality checks, lineage for regulatory reports, RACI documented | Governance council meets quarterly | Moderate, gaps in real-time monitoring |

| 4 | Managed | KPI-driven governance, real-time dashboards, federated model operational, automated policy enforcement, integrated security monitoring | Metrics-driven decisions, automated alerting | Low, predictive capabilities missing |

| 5 | Optimized | AI-driven autonomous governance, predictive compliance, continuous audit readiness, self-healing data quality, full data ethics integration | Governance embedded in all data products | ✅ Minimal, industry-leading |

Self-Assessment Scoring Matrix

Rate your institution 1–5 on each dimension:

| # | Capability Dimension | Score (1–5) |

|---|---|---|

| 1 | Data cataloging coverage | _ |

| 2 | Lineage documentation completeness | _ |

| 3 | Quality management automation | _ |

| 4 | Access control maturity | _ |

| 5 | Policy automation level | _ |

| 6 | Stewardship effectiveness | _ |

| 7 | Security monitoring integration | _ |

Average score = current maturity level.

| Average | Interpretation |

|---|---|

| Below 2.0 | ❌ Immediate remediation needed |

| 2.0–3.0 | Foundation exists; invest in automation |

| 3.0–4.0 | Strong foundation; focus on AI-driven optimization |

| 4.0+ | ✅ Industry-leading; focus on predictive and autonomous capabilities |

💰 ROI Framework by Maturity Transition

| Transition | Typical Investment | Expected Return |

|---|---|---|

| Level 1 → 2 | $500K–$2M | Prevents $5M–$15M in annual poor-data-quality costs |

| Level 2 → 3 | $1M–$5M | Reduces audit remediation costs by 40–60%; accelerates regulatory reporting by weeks |

| Level 3 → 4 | $2M–$8M | Enables real-time compliance monitoring; eliminates 200+ person-hours per audit exam |

| Level 4 → 5 | $3M–$10M+ | Predictive compliance; governance embedded in every data product and AI pipeline |

Benchmarks by Institution Size

| Institution Type | Typical Maturity (2026) | Target Maturity | Governance Budget (% of IT spend) |

|---|---|---|---|

| Community Bank | 1.5–2.0 | 3.0 | 2–4% |

| Regional Bank | 2.0–3.0 | 4.0 | 3–5% |

| Global SIFI | 3.0–3.5 | 4.5+ | 5–8% |

| Fintech (Series B+) | 1.5–2.5 | 3.5 | 4–6% |

Governance ROI is measurable through specific KPIs: time-to-audit-readiness, regulatory finding reduction rate, data quality scores, and incident response time for governance violations. The institutions that track these metrics quarterly are the ones advancing through maturity levels; the ones that only measure during exam season stay stuck. For organizations looking to quantify their cybersecurity budget against governance maturity targets, benchmarking against these ranges provides a defensible starting point.

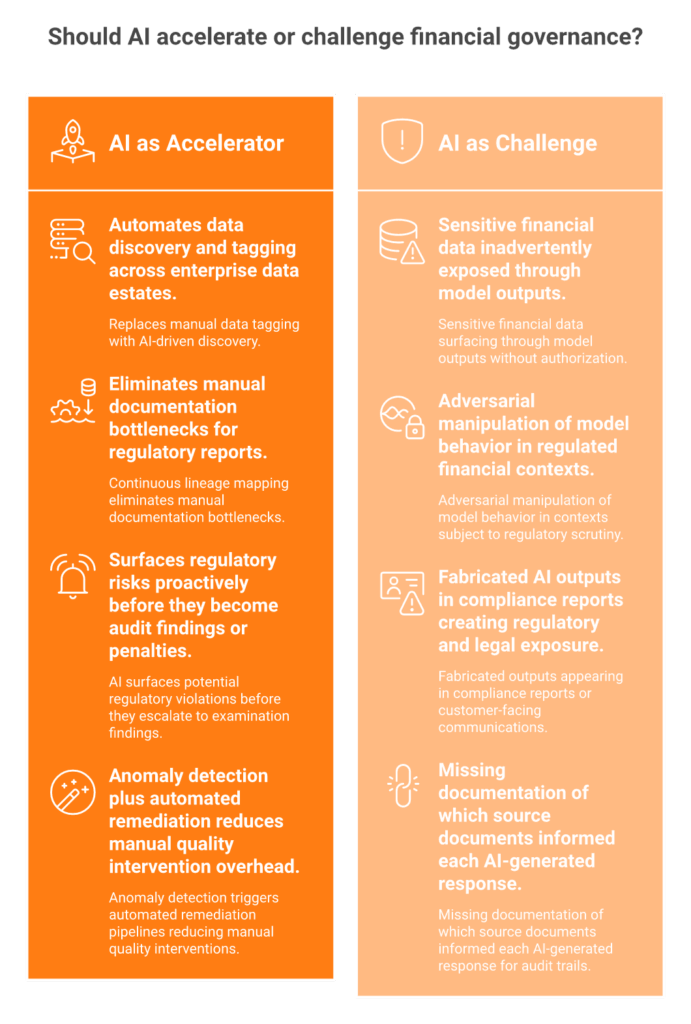

Q8. How Is AI Transforming Data Governance and What Does LLM-Era Model Risk Look Like?

Financial institutions are deploying AI at unprecedented scale: credit scoring, fraud detection, algorithmic trading, customer service chatbots, and AML monitoring. Yet governance has not kept pace. Roughly 55% of financial institutions still lack formal AI governance frameworks. The data feeding these models is often governed by one team, the models by another, and security monitoring by a third. This fragmentation means ungoverned training data flows into production AI systems, model outputs lack explainability audit trails, and drift goes undetected until regulatory findings surface.

❌ Why Traditional Approaches Fall Short

Current governance frameworks treat AI as an afterthought, bolting model risk management onto existing data governance rather than integrating them architecturally. Rule-based compliance monitoring can’t keep pace with model drift, adversarial attacks on financial AI, or the rapid iteration cycles of ML deployment.

OCC examiners are now rejecting black-box AI models during SR 11-7 validation, even when those models outperform traditional logistic regression scorecards on every performance metric. The Comptroller’s Handbook explicitly requires that model logic “can be reasonably understood by qualified individuals.” The Bank of England’s SS1/23 guidance demands continuous validation that manual processes cannot deliver at scale. Most financial institutions still manage model inventories in spreadsheets, a practice incompatible with the velocity of modern AI deployment.

AI as Both Tool and Challenge

On the tool side: AI-driven governance automates data classification, real-time lineage tracking, predictive compliance alerts, intelligent data quality monitoring, and anomaly detection at a scale no human team can match. This is where the maturity jump from Level 3 to Level 4 happens, as automation replaces manual governance processes.

On the challenge side: Governing training data for credit scoring requires documented provenance, bias testing, and fairness validation across protected classes. The EU AI Act classifies financial AI (credit, insurance pricing, and fraud detection) as “high-risk,” mandating governed training data, bias documentation, explainability audits, human oversight mechanisms, and post-deployment monitoring.

⚠️ LLM-Specific Governance: The 2026 Frontier

Financial institutions deploying LLMs for document processing, customer interaction, and internal knowledge management face governance challenges that existing frameworks weren’t designed for:

- Prompt injection risks: Adversarial inputs that manipulate model behavior in regulated contexts

- Output traceability: Every AI-generated response used in regulatory contexts needs an audit trail

- Training data leakage: Preventing sensitive financial data from surfacing in model outputs

- Hallucination risk: Fabricated outputs in compliance reports or customer-facing communications

- RAG source attribution: Documenting which source documents informed each generated response

Model Governance Requirements Matrix

| Component | Requirement | Primary Regulation |

|---|---|---|

| Model Inventory | Registry of all AI/ML models with risk classifications | OCC SR 11-7 |

| Performance Monitoring | Automated drift detection, accuracy tracking, fairness metrics | EU AI Act, SS1/23 |

| Governance Controls | Access controls on training data, explainability documentation, bias mitigation | BCBS 239, GDPR |

| LLM-Specific | Prompt logging, output versioning, RAG source attribution, DLP integration | EU AI Act, SEC Rule 204-2 |

The Security Bridge

Where governance frameworks define what AI data should be protected and how, continuous security operations ensure those protections hold in practice. Unauthorized access to training datasets, data poisoning attacks, and model extraction attempts require real-time security monitoring that governance policies alone cannot provide. Financial institutions need integrated security operations that detect anomalous access to AI training data and governed datasets around the clock, not just governance documentation describing the ideal state.

The operational reality: governance without enforcement is a policy binder on a shelf. Enforcement without governance is security theater. The institutions that integrate both, through automated governance policies monitored by continuous security operations for financial services, are the ones that will pass the next AI-focused regulatory examination.

Q9. What Are the Biggest Data Governance Challenges and How Do Financial Institutions Overcome Them?

Your compliance team receives an SEC examination notice targeting electronic communications governance. Examiners want proof that business-related messages on WhatsApp, personal email, and SMS are captured, archived, and searchable. Your official policy prohibits off-channel communications. Your reality: traders use WhatsApp daily, relationship managers text clients, and the compliance team has no visibility. You’re now joining 100+ financial firms that paid $3B+ in SEC fines for exactly this governance gap.

That scenario isn’t rare but rather the norm. Here are the eight challenges that derail governance programs, along with the resolution paths that actually work.

Challenge 1–4: Structural and Organizational

| # | Challenge | Root Cause | Resolution |

|---|---|---|---|

| 1 | Data Silos across retail, commercial, and investment banking | Independent technology stacks, competing business priorities | Federated governance with a unified catalog and cross-domain data stewards |

| 2 | Legacy Systems & Technical Debt | Decades of accumulated infrastructure with no lineage capability | API-based integration layers with automated lineage extraction; phased modernization roadmap. Don’t try to boil the ocean. |

| 3 | Data Volume, Velocity, and Complexity | Streaming data, real-time transactions, and IoT telemetry outpacing batch governance | Streaming data governance frameworks, real-time quality monitoring, and event-driven architecture governance |

| 4 | Cultural Resistance & Ownership Gaps | Governance perceived as “compliance overhead,” not business value | Embed governance into existing workflows (not overlay); executive sponsorship; demonstrate value through quick wins on regulatory reporting speed |

Challenge 5–8: Operational and Regulatory

| # | Challenge | Root Cause | Resolution |

|---|---|---|---|

| 5 | Shadow Data & Shadow IT | Ungoverned copies in departmental spreadsheets, personal drives, and unsanctioned SaaS | Automated discovery tools, regular data estate scanning, and governance-by-design in provisioning workflows |

| 6 | ⚠️ Retention vs. Deletion Conflicts | GDPR says delete; SEC says retain for seven years. Mandates directly conflict. | Jurisdiction-aware retention policy engine applying the most restrictive requirement; purpose-based retention with documented legal basis for every data category |

| 7 | ❌ Off-Channel Communication Governance | Business communications happening on unauthorized platforms with zero capture | Deploy communication capture platforms, enforce acceptable-use policies with technical controls, and conduct regular compliance testing |

| 8 | Manual Remediation Costs | Human-dependent quality checks, lineage documentation, and audit preparation | Automate quality validation gates, implement self-healing data quality pipelines, and reduce manual touchpoints through policy automation |

💸 The Hidden Cost Quantification

The operational impact of these challenges compounds fast:

- Manual lineage documentation costs 200+ person-hours per regulatory exam

- Data quality issues cause 15–25% of regulatory report resubmissions

- Cultural resistance extends governance program timelines by 12–18 months

- Shadow data accounts for an estimated 30–40% of enterprise data estates and is the top source of audit findings

The common thread across all eight challenges is the gap between governance policy and operational enforcement. Institutions write policies that describe the ideal state. Examiners test the actual state. The gap between the two is where fines, findings, and breaches live. Closing it requires both automated governance tools and continuous security monitoring to ensure policies are upheld in practice, not just documented in a binder.

Q10. What Tools and Technologies Power Financial Data Governance in 2026?

Financial data governance in 2026 runs on an ecosystem of specialized and integrated platforms spanning eight capability categories. The right technology selection depends on your institution’s maturity level, existing stack, and regulatory exposure, not on vendor marketing claims.

Technology Capability Map

| # | Category | Representative Platforms | Primary Function |

|---|---|---|---|

| 1 | Data Catalogs & Metadata Management | Collibra, Alation, Atlan, OvalEdge | Enterprise data inventory with business context and automated discovery |

| 2 | Data Lineage & Traceability | Collibra Lineage, Manta, Informatica | End-to-end data flow mapping from source to regulatory report |

| 3 | Data Quality Monitoring | Great Expectations, Monte Carlo, Ataccama | Automated profiling, validation, anomaly detection, and quality scoring |

| 4 | AI-Driven Governance Automation | Emerging capabilities across platform vendors | Auto-classification, policy enforcement, and predictive compliance alerts |

| 5 | Cloud Governance | AWS Lake Formation, Azure Purview, GCP Dataplex | Hybrid/multi-cloud access control, classification, and policy management |

| 6 | Communication Governance | LeapXpert, Global Relay, Smarsh | Off-channel capture, archive, and surveillance for regulatory compliance |

| 7 | ESG Data Governance | Specialized ESG platforms | ESG data quality validation, SFDR/CSRD reporting consistency |

| 8 | Streaming Data Governance | Schema registries, data contracts platforms | Event-driven architecture governance, real-time policy enforcement |

✅ Vendor-Neutral Evaluation Criteria

When evaluating governance technology, score each platform against these seven dimensions:

- Integration Breadth: Does it connect to your existing data infrastructure without requiring rip-and-replace? Vendor lock-in in governance tools is just as dangerous as in security tools.

- Automation Level: Can it auto-discover, classify, and apply policies without manual configuration for each asset?

- Regulatory Mapping: Does it include pre-built templates for BCBS 239, GDPR, DORA, and SOX?

- Lineage Depth: Column-level and transformation-level lineage, or just table-level? The difference matters when an examiner asks “where did this number come from?”

- Security Integration: Does governance monitoring connect with security operations for real-time enforcement?

- Scalability: Can it handle enterprise data volumes across cloud and on-prem environments?

- Audit Evidence Generation: Does it automatically produce the documentation regulators require?

⏰ Emerging Trends Reshaping the Landscape

Three shifts are redefining what governance technology looks like:

- AI-driven autonomous governance: Self-classifying data assets, self-healing data quality, and AI-generated policy recommendations are moving from experimental to production-ready.

- Metadata control planes: A unified metadata layer serving as the single source of truth for governance, quality, lineage, and security, replacing the patchwork of disconnected tools.

- Governance-observability convergence: The line between data governance platforms and data observability tools is dissolving. The next generation of platforms combines policy enforcement with real-time pipeline monitoring in a single operational layer.

The most significant shift is architectural: standalone governance tools are giving way to integrated platforms that combine governance, quality, security, and compliance. Institutions still buying point solutions for each capability will spend the next two years integrating them, and that is time most governance programs don’t have.

Q11. How Does Continuous Security Monitoring Protect Governed Data in Financial Services?

Data governance frameworks define what data must be protected and how. Without continuous security monitoring, those policies exist on paper while unauthorized access, exfiltration, and integrity violations go undetected. The enforcement gap between governance policy and operational reality is where financial institutions are most vulnerable to both breaches and audit findings.

Why Regulators Now Link Governance to Security Operations

In 2026, regulators explicitly connect governance effectiveness to security operations. DORA requires ICT incident detection and reporting within hours. BCBS 239 expects data integrity controls to function continuously, not just during audit periods. The institutions that pass regulatory examinations consistently are those where governance policies are enforced by real-time security monitoring, not manual periodic reviews.

✅ What Governance-Aware Security Monitoring Looks Like

Not all security monitoring is built to enforce governance. Here’s what separates governance-aware solutions from generic tools:

- Vendor-agnostic integration spanning the entire governed data estate regardless of technology stack: SIEM, EDR, cloud, and identity platforms connected into a single detection layer

- Real-time detection of governance policy violations, including unauthorized data access, privilege escalations, and anomalous query patterns on sensitive financial data

- Human analyst verification of flagged data access to confirm whether activity is legitimate or a policy breach, not just an automated alert that gets lost in a queue

- Automated audit trail generation for compliance evidence that regulators can review

- Incident response capability that contains governance violations within minutes, not hours

“They’ve also made our audit process much less painful. The reports from their platform give us clear evidence of our security controls and incident response capabilities. When auditors or clients ask questions about our security posture, we can pull up exactly what they need to see.”

— Verified User, Marketing and Advertising UnderDefense – G2 Verified Review

“UnderDefense MAXI integrates well with our systems, specifically with our SIEM, Splunk. Their team is proactive in identifying and addressing threats, providing 24/7 oversight.”

— Oleg K., Director Information Security UnderDefense – G2 Verified Review

The Right Partner Makes Governance Enforceable

The right security monitoring partner integrates with your governance infrastructure to enforce policies 24/7, detecting unauthorized access to governed data assets, verifying anomalous activity directly with users via ChatOps, and generating the audit evidence regulators require. For financial institutions building audit-ready governance frameworks, the security operations layer determines whether your governance investment delivers protection or just documentation.

This analysis is grounded in documented response times, regulatory examination outcomes, and operational case studies across financial institutions, including incident response and post-breach recovery cases documented by UnderDefense.

Q12. What Future Trends Will Reshape Data Governance in Financial Services Beyond 2026?

Governance isn’t standing still. The institutions that treat their current framework as “done” will find it outdated within 18 months. Here are seven trends already reshaping the landscape.

7 Trends Shaping the Next Era

- AI-Driven Autonomous Governance: Self-classifying data assets, self-healing quality pipelines, and AI-generated policy recommendations that reduce manual governance overhead by 50%+

- Real-Time Continuous Compliance Monitoring: The shift from periodic audits to always-on regulatory dashboards. Regulators are piloting supervisory technology that monitors model behavior and data integrity directly.

- Data Democratization with Governed Self-Service: Enabling business users to access data freely within governance guardrails, using automated policy enforcement to replace manual approval bottlenecks

- Cloud-Native Governance Expansion: Governance built into cloud infrastructure (lakehouses, data meshes) rather than bolted on top

- Data Ethics as Strategic Priority: Beyond compliance to ethical data use as competitive differentiator and board-level concern, driven by EU AI Act fairness requirements

- Metadata Control Planes: Unified metadata layer as the single source of truth for governance, quality, lineage, and security across the entire data estate

- Governance-Observability Convergence: Merging governance policy enforcement with real-time data pipeline observability into a single operational layer

⭐ Quantified Case Study Snapshots

- Global Insurer: Achieved audit-ready governance across 15 jurisdictions within 6 weeks of deploying automated lineage and catalog tools, reducing audit preparation time by 70%

- Digital Bank: Governance-by-design approach enabled 3x faster product launches by eliminating governance bottlenecks in data pipeline approvals

- Lending Fintech: Automated data quality gates and governance policies saved 200+ engineering hours monthly by eliminating manual data remediation workflows

FAQ: Data Governance in Financial Services

What is data governance in financial services?

Data governance in financial services is the system of policies, roles, standards, and technologies ensuring financial data is accurate, secure, traceable, and compliant throughout its lifecycle, covering everything from customer PII to AI model outputs.

What regulations require data governance in banking?

Key regulations include BCBS 239, GDPR, SOX, GLBA, DORA, PCI-DSS, Basel III, MiFID II, 23 NYCRR 500, EU AI Act, and SEC recordkeeping rules, each imposing specific data lineage, quality, access, and retention requirements.

What is BCBS 239 and how does it relate to data governance?

BCBS 239 is the Basel Committee’s standard for risk data aggregation and reporting. It requires banks to demonstrate data accuracy, completeness, timeliness, and traceability across all risk reports, making it the foundational governance regulation for banking.

What is a data governance maturity model for financial institutions?

A 5-level framework (Ad Hoc → Developing → Standardized → Managed → Optimized) aligned with DCAM and DAMA-DMBOK that measures governance capabilities across cataloging, lineage, quality, access controls, and policy automation.

How does DORA affect data governance in 2026?

DORA mandates ICT resilience, data integrity during disruptions, incident reporting within hours, and third-party ICT risk governance, requiring financial entities to maintain governed, auditable data across all operational systems.

What is the difference between data governance for banks and fintechs?

Banks face legacy system integration and dense prudential regulation (Basel, BCBS 239). Fintechs deal with hypergrowth, API-first architectures, and evolving mandates like PSD3, though requirements converge as fintechs mature.

How does AI change data governance in financial services?

AI simultaneously accelerates governance (automated classification, real-time lineage, and predictive compliance) and creates new governance demands (training data provenance, bias documentation, and model explainability under the EU AI Act).

What tools are used for financial data governance?

Core categories include data catalogs (Collibra, Alation), lineage tools (Manta, Informatica), quality platforms (Monte Carlo, Ataccama), cloud governance (AWS Lake Formation, Azure Purview), and communication governance platforms.

1. What is data governance in financial services and why is it critical in 2026?

Data governance in financial services is the system of policies, roles, standards, metrics, and technologies that ensures financial data is accurate, secure, traceable, and compliant throughout its entire lifecycle. It spans every asset from customer PII to AI model outputs.

In 2026, data governance has reached an inflection point because multiple regulatory timelines are converging simultaneously. DORA is now in active enforcement with fines reaching up to 10% of annual turnover, and only an estimated 50% of financial institutions are fully compliant. The EU AI Act classifies financial AI systems like credit scoring and fraud detection as high-risk, requiring governed training data and explainability audits. GDPR enforcement continues to intensify, Basel III Endgame is reshaping capital adequacy data requirements, and cross-border data sovereignty mandates are adding new layers of complexity.

We see governance as the foundation that answers the one question every regulator will eventually ask: can you prove your data is trustworthy? For institutions navigating these overlapping mandates, a compliance roadmap that maps governance controls to specific regulations is no longer optional.

2. What does poor data governance actually cost banks and financial institutions?

The financial impact of poor data governance compounds across multiple dimensions. Gartner estimates poor data quality costs organizations an average of $12.9–$15 million per year. In financial services, where data drives every risk decision and regulatory filing, the cost categories include:

-

Regulatory penalties: GDPR single fines have reached up to €1.2B, and the SEC has levied over $3B in cumulative off-channel communication fines since 2021.

-

Audit remediation: Manual lineage documentation alone costs 200+ person-hours per regulatory exam.

-

Operational waste: Employees spend up to 27% of their time correcting bad data.

-

Reputational damage: Stock price drops, customer attrition, and board-level consequences.

Real-world failures like Equifax ($700M settlement), Capital One ($80M OCC fine), and Danske Bank’s €200B AML scandal all trace back to governance gaps. Executive liability is also rising under the UK’s SM&CR regime, making governance a personal, career-defining risk. We help leaders quantify this exposure using our cybersecurity budget playbook to frame governance investment as revenue protection.

3. Which regulations drive data governance requirements for banks and fintechs?

Financial institutions in 2026 face overlapping mandates across at least 14 active regulations. The most impactful include:

-

BCBS 239: The foundational governance regulation for banking, requiring risk data aggregation accuracy, completeness, and traceability.

-

DORA: In enforcement since January 2025, mandating ICT resilience, data integrity during disruptions, and incident reporting within 4 hours.

-

EU AI Act: Classifies financial AI (credit scoring, fraud detection, insurance pricing) as high-risk, requiring governed training data, bias documentation, and explainability audits.

-

GDPR/CPRA: Data protection, consent management, and retention/deletion obligations.

-

SEC Rule 204-2: Recordkeeping and communication retention, with $3B+ in cumulative fines for off-channel violations.

-

SOX: Financial reporting data integrity and internal controls.

The challenge isn’t understanding any single regulation but managing the convergence. We help institutions preparing for DORA penetration testing close compliance gaps before examination windows shrink further.

4. How do you build an audit-ready data governance framework step by step?

We recommend an 8-step implementation roadmap where every step maps directly to the audit evidence it produces:

-

Define governance objectives, scope, and success metrics tied to business outcomes.

-

Secure executive buy-in by framing governance as revenue protection.

-

Conduct a data landscape assessment across on-prem, cloud, SaaS, and shadow IT.

-

Prioritize Critical Data Elements (CDEs) starting with regulatory-critical data.

-

Establish the CDO office, governance council, and RACI-mapped stewardship roles.

-

Build governance policies, a business glossary, and SOPs.

-

Select and deploy governance technology (catalog, lineage, quality, access control).

-

Implement continuous monitoring, training, and refinement cycles.

Institutions scoring below 5 on our 8-point audit-readiness checklist should prioritize automated governance platforms before the next examination window. The cost of manual remediation after an examiner identifies deficiencies is 3–5x higher than proactive implementation.

5. What does a data governance maturity model look like for financial institutions?

The industry-standard maturity model uses five levels aligned with DCAM (developed by the EDM Council specifically for financial services) and DAMA-DMBOK:

-

Level 1 (Ad Hoc): No formal governance, reactive compliance, tribal knowledge. High penalty exposure.

-

Level 2 (Developing): Basic policies, data owners assigned, catalog covers less than 40% of CDEs.

-

Level 3 (Standardized): Enterprise-wide framework operational, automated quality checks, RACI documented.

-

Level 4 (Managed): KPI-driven governance, real-time dashboards, automated policy enforcement.

-

Level 5 (Optimized): AI-driven autonomous governance, predictive compliance, continuous audit readiness.

Most financial institutions in 2026 operate at Level 2–3. The jump from Level 3 to Level 4 is where AI-driven automation becomes critical. ROI is measurable: a Level 1-to-2 transition ($500K–$2M investment) prevents $5M–$15M in annual poor-data-quality costs.

6. How is AI transforming data governance and what are LLM-specific risks?

AI serves as both a governance accelerator and a new governance challenge. On the tool side, AI-driven governance automates data classification, real-time lineage tracking, predictive compliance alerts, and anomaly detection at a scale no human team can match.

On the challenge side, roughly 55% of financial institutions still lack formal AI governance frameworks. The EU AI Act classifies financial AI as high-risk, mandating governed training data, bias documentation, explainability audits, and post-deployment monitoring. LLM-specific risks include:

-

Prompt injection attacks manipulating model behavior in regulated contexts

-

Output traceability gaps for AI-generated responses in regulatory contexts

-

Training data leakage exposing sensitive financial data

-

Hallucination risk producing fabricated outputs in compliance reports

-

RAG source attribution gaps lacking documentation of which sources informed each response

OCC examiners are now rejecting black-box AI models during SR 11-7 validation. Financial institutions need integrated security operations that detect anomalous access to AI training data and governed datasets around the clock.

7. How does continuous security monitoring protect governed financial data?

Data governance frameworks define what data must be protected and how, but without continuous security monitoring, those policies exist on paper while unauthorized access and integrity violations go undetected. In 2026, regulators explicitly connect governance effectiveness to security operations. DORA requires ICT incident detection and reporting within hours. BCBS 239 expects data integrity controls to function continuously, not just during audit periods.

Governance-aware security monitoring includes:

-

Vendor-agnostic integration spanning the entire governed data estate (SIEM, EDR, cloud, identity platforms)

-

Real-time detection of governance policy violations, including unauthorized data access and privilege escalations

-

Human analyst verification of flagged access to distinguish legitimate activity from policy breaches

-

Automated audit trail generation for compliance evidence

-

Incident response capability that contains governance violations within minutes

The operational reality: governance without enforcement is a policy binder on a shelf. The institutions that integrate automated governance policies with continuous security operations are the ones passing the next regulatory examination.

8. What tools and technologies power financial data governance in 2026?

Financial data governance in 2026 runs on eight capability categories of specialized and integrated platforms:

-

Data catalogs: Collibra, Alation, Atlan, OvalEdge for enterprise data inventory with business context.

-

Data lineage: Collibra Lineage, Manta, Informatica for end-to-end data flow mapping.

-

Data quality: Great Expectations, Monte Carlo, Ataccama for automated validation and anomaly detection.

-

AI-driven governance automation: Emerging auto-classification and predictive compliance capabilities.

-

Cloud governance: AWS Lake Formation, Azure Purview, GCP Dataplex for hybrid/multi-cloud policy management.

-

Communication governance: LeapXpert, Global Relay, Smarsh for off-channel capture and surveillance.

-

ESG and streaming data governance for specialized reporting and event-driven architectures.

When evaluating platforms, we recommend scoring against seven dimensions: integration breadth, automation level, regulatory mapping, lineage depth, security integration, scalability, and audit evidence generation. Vendor lock-in in governance tools is just as dangerous as in security tools. The most significant architectural shift is standalone governance tools giving way to integrated platforms combining governance, quality, security, and compliance.